The amounts of compensation subject to Railroad Retirement Tier I and Tier II payroll taxes will go up in 2023, while the tax rates on employers and employees will stay the same. In addition, unemployment insurance contribution rates paid by railroad employers will include a surcharge of 1.5%, down from 3.5% in 2022, due to an improved employment outlook since the beginning of the pandemic.

Tier I and Medicare Tax — The Railroad Retirement Tier I payroll tax rate on covered rail employers and employees for 2023 remains at 7.65%. The Railroad Retirement Tier I tax rate is the same as the Social Security tax, and for withholding and reporting purposes is divided into 6.20% for retirement and 1.45% for Medicare hospital insurance. The maximum amount of an employee’s earnings subject to the 6.20% rate increases from $147,000 to $160,200 in 2023, with no maximum on earnings subject to the 1.45% Medicare rate.

An additional Medicare payroll tax of 0.9% applies to an individual’s income exceeding $200,000, or $250,000 for a married couple filing a joint tax return. While employers will begin withholding the additional Medicare tax as soon as an individual’s wages exceed the $200,000 threshold, the final amount owed or refunded will be calculated as part of the individual’s federal income tax return.

Tier II Tax — The Railroad Retirement Tier II tax rates in 2023 will remain at 4.9% for employees and 13.1% for employers. The maximum amount of earnings subject to Railroad Retirement Tier II taxes in 2023 will increase from $109,200 to $118,800. Tier II tax rates are based on an average account benefits ratio reflecting Railroad Retirement fund levels. Depending on this ratio, the Tier II tax rate for employees can be between 0% and 4.9%, while the Tier II rate for employers can range between 8.2% and 22.1%.

Unemployment Insurance Contributions — Employers, but not employees, pay railroad unemployment insurance contributions, which are experience-rated by employer. The Railroad Unemployment Insurance Act (RUIA) also provides for a surcharge in the event the Railroad Unemployment Insurance Account balance falls below an indexed threshold amount. The accrual balance of the Railroad Unemployment Insurance Account was $112.7 million on June 30, 2022. Since the balance was below the indexed $100 million threshold (currently $137.9 million), but above the $50 million indexed threshold (currently $67.0 million), this results in a 1.5% surcharge in 2023. There was a surcharge of 3.5% in 2022 and 2.5% in 2021.

As a result, the unemployment insurance contribution rates on railroad employers in 2023 will range from the minimum rate of 2.15% to the maximum of 12.0% on monthly compensation up to $1,895, an increase from $1,755 in 2022.

In 2023, the minimum rate of 2.15% will apply to 80% of covered employers, with 6% paying the maximum rate of 12.0%. New employers will pay an unemployment insurance contribution rate of 2.82%, which represents the average rate paid by all employers in the period 2019-2021.

Tax Type

Rate – Employee

Rate – Employer

Annual Taxable Maximum

Annual Tax Amount Employer

Tier 1 – Medicare*

1.45%

1.45%

No Maximum

No Maximum

Tier 1 – Railroad Retirement

6.20%

6.20%

$160,200.00

$9,932.40

Tier 2 – Railroad Retirement

4.90%

13.10%

$118,800.00

$15,562.80

Total

12.55%

20.75%

$25,495.20

*Additional Medicare Tax: Employees will pay an additional 0.9% Medicare Tax on earnings above $200,000 (for those who file an individual return) or $250,000 (for those who file a joint return). This additional Medicare tax rate is not reflected in the tax rates shown above.

Note: Tier 1 Medicare and Tier 1 Railroad Retirement tax rates are equivalent to Social Security tax rates set for 2023. Tier 2 Railroad Retirement tax rates do not apply to employees subject to Social Security.

Below are PDFs of various releases from the RRB on 2023 tax rates:

Many railroad employees have served in the Armed Forces of the United States. Under certain conditions, their military service may be creditable as railroad service under the Railroad Retirement Act (RRA).

The following questions and answers provide information on how military service may be credited toward Railroad Retirement benefits.

1. Under what conditions can military service be credited as railroad service?

The intent behind the crediting of military service under the RRA is to prevent career railroad employees from losing retirement credits while performing active-duty military service during a war or national emergency period. Therefore, to be creditable as compensation under the RRA, service in the U.S. Armed Forces must be preceded by railroad service in the same or preceding calendar year. With the exceptions noted later, the employee must also have entered military service when the United States was at war or in a state of national emergency, or have served in the armed forces involuntarily. Military service is involuntary when an employee is required by law, such as Selective Service System conscription or troop call-up from a reserve unit, to leave railroad service to perform active duty military service.

Only active-duty military service is creditable under the RRA. A person is considered to have been on active duty while commissioned, or enrolled, in the active service of the Armed Forces of the United States (including the U.S. Coast Guard), or while ordered to federal active duty from any reserve component of the uniformed armed forces.

2. What are some examples of creditable service performed by a member of a reserve component, such as the Army Reserve?

Any military service a reservist is required to perform as a result of a call-up to active duty, such as during a partial mobilization, is creditable under the RRA, so long as the military service is preceded by railroad service in the same or preceding year.

Annual training duty as a member of a reserve component of a uniformed service is also considered active duty and may be creditable, provided the railroad employee service requirement is met. The period of active duty for training also includes authorized travel time to and from any such training duty. However, weekend alone or evening reserve duty is not creditable.

Active duty in a state National Guard or state Air National Guard unit may be creditable only while the reservist was called to federal active duty by Congress or the president of the United States. Emergency call-up of the National Guard by a governor for riot or flood control would not be creditable.

3. What are the dates of the war or national emergency periods?

The war or national emergency periods are:

August 2, 1990, to date as yet undetermined.

December 16, 1950, through September 14, 1978.

September 8, 1939, through June 14, 1948.

If military service began during a war or national emergency period, any active duty service the employee was required to continue in beyond the end of the war or national emergency is creditable, except that voluntary service extending beyond September 14, 1978, is not creditable.

Railroad workers who voluntarily served in the armed forces between June 15, 1948, and December 15, 1950, when there was no declared national state of emergency, can be given Railroad Retirement credit for their military service if they:

performed railroad service in the year they entered or the year before they entered military service, and;

returned to rail service in the year their military service ended, or in the following year, and;

had no intervening nonrailroad employment.

4. How can military service be used to increase benefits paid by the Railroad Retirement Board (RRB)?

Railroad Retirement annuities are based on length of service and earnings. If military service is creditable as railroad service, a person will receive additional compensation credits for each month of creditable military service and railroad service credit for each active military service month not already credited by actual railroad service.

Creditable military service may be used in addition to regular railroad service to meet certain service requirements, such as the basic 10-year or 5-year service requirements for a regular annuity, the 20-year requirement for an occupational disability annuity before age 60, the 25-year requirement for a supplemental annuity, or the 30-year requirement for early retirement benefits.

5. Can United States Merchant Marine service be creditable for Railroad Retirement purposes?

No. Service with the Merchant Marine or civilian employment with the Department of Defense is not creditable, even if performed in wartime.

6. Are Railroad Retirement annuities based in part on military service credits reduced if other benefits, such as military service pensions or payments from the Department of Veterans Affairs, are also payable on the basis of the same military service?

No. While Railroad Retirement employee annuities are subject to reductions for dual entitlement to Social Security benefits and, under certain conditions, federal, state or local government pensions, as well as certain other payments, Railroad Retirement employee annuities are always exempt from reduction for military service pensions or payments by the Department of Veterans Affairs.

7. Are the unemployment and sickness benefits payable by the RRB affected if an employee is also receiving a military service pension?

Yes. The unemployment and sickness benefits payable by the RRB are affected if a claimant is also receiving a military service pension. However, payments made by the Department of Veterans Affairs will not affect railroad unemployment or sickness benefits.

When a claimant is receiving a military service pension or benefits under any social insurance law for days in which he or she is entitled to benefits under the Railroad Unemployment Insurance Act, railroad unemployment or sickness benefits are payable only to the extent to which they exceed the other payments for those days. In many cases, the amount of a military service pension precludes the payment of unemployment or sickness benefits by the RRB. Examples of other such social insurance payments are firefighters’ and police pensions, or certain workers’ compensation payments. Claimants should report all such payments promptly to avoid having to refund benefits later.

8. Can proof of military service be filed in advance of retirement?

Yes. Railroad employees are encouraged to file their military service proofs well before retirement to expedite the annuity application process and avoid delays caused by inadequate proofs. Proofs can be mailed to an employee’s local RRB field office, or placed in the secure lockboxes/door slots outside of an RRB field office’s doors. (Lockboxes and door slots are checked daily.) Employee information will be recorded and stored electronically until an employee retires. All evidence brought or mailed to an RRB office will be handled carefully and returned promptly.

If employees do not have an official record of their military service, their local RRB office will explain how to get acceptable evidence.

9. How can an employee get more information about the crediting of his or her military service by the RRB?

More information is available by visiting the RRB’s website, RRB.gov, or by calling an RRB office toll-free at 1-877-772-5772. Persons can find the address of the RRB office servicing their area by calling the agency’s toll-free number or by clicking on the Field Office Locator tab at RRB.gov. RRB field offices currently offer limited in-person service by appointment. To schedule an appointment, call 1-877-772-5772. Individuals should bring a photo ID when visiting a field office, and, depending on guidance from the Centers for Disease Control and Prevention for the county in which the field office is located, may be required to wear an appropriate face mask. In such circumstances, if visitors do not have a mask, one will be provided for them.

Railroad Retirement annuitants subject to earnings restrictions can earn more in 2023 without having their benefits reduced due to increased limits indexed to average national wage increases.

Like Social Security benefits, some Railroad Retirement benefit payments are subject to deductions if an annuitant’s earnings exceed certain exempt amounts. These earnings restrictions apply to those who have not attained full Social Security retirement age. For employee and spouse annuitants, full retirement age varies depending on an individual’s year of birth, and is age 67 for those born after 1959. For survivor annuitants, full retirement age also varies, and is age 67 for those born after 1961.

For those under full retirement age throughout 2023, the exempt earnings amount rises to $21,240 from $19,560 in 2022. For beneficiaries attaining full retirement age in 2023, the exempt earnings amount, for the months before the month full retirement age is attained, increases to $56,520 in 2023 from $51,960 in 2022.

For those under full retirement age, the earnings deduction is $1 in benefits for every $2 of earnings over the exempt amount. For those attaining full retirement age in 2023, the deduction is $1 for every $3 of earnings over the exempt amount in the months before the month full retirement age is attained.

When applicable, these earnings deductions are assessed on the Tier I portion of Railroad Retirement employee and spouse annuities, and the Tier I and Tier II portions of survivor benefits.

All earnings received for services rendered, plus any net earnings from self-employment, are considered when assessing deductions for earnings. Interest, dividends, certain rental income or income from stocks, bonds or other investments are not considered earnings for this purpose.

Retired employees and spouses, regardless of age, who work for their last pre-retirement non-railroad employer are also subject to an additional earnings deduction, in their Tier II and supplemental benefits, of $1 for every $2 in earnings up to a maximum reduction of 50%. This earnings restriction does not change from year to year and does not allow for an exempt amount.

A spouse benefit is subject to reduction not only for the spouse’s earnings, but also for the earnings of the employee, regardless of whether the earnings are from service for the last pre-retirement non-railroad employer or other post-retirement employment.

Special work restrictions continue to be applicable to disability annuitants in 2023. The monthly disability earnings limit increases to $1,150 in 2023 from $1,050 in 2022.

Regardless of age and/or earnings, no Railroad Retirement annuity is payable for any month in which an annuitant (retired employee, spouse or survivor) works for a railroad employer or railroad union.

Most Railroad Retirement annuities, like Social Security benefits, will increase in January 2023 due to a rise in the Consumer Price Index (CPI) from the third quarter of 2021 to the corresponding period of the current year.

Cost-of-living increases are calculated in both the Tier I and Tier II portion of a Railroad Retirement annuity. Tier I benefits, like Social Security benefits, will increase by 8.7%, which is the percentage of the CPI rise. This is the largest increase since 1981, when it was 11.2%.

Tier II benefits will go up by 2.8%, which is 32.5% of the CPI increase. Vested dual benefit payments and supplemental annuities also paid by the Railroad Retirement Board (RRB) are not adjusted for the CPI change.

In January 2023, the average regular Railroad Retirement employee annuity will increase $215 a month to $3,344 and the average of combined benefits for an employee and spouse will increase $304 a month to $4,838. For those aged widow(er)s eligible for an increase, the average annuity will increase $120 a month to $1,691.

Widow(er)s whose annuities are being paid under the Railroad Retirement and Survivors’ Improvement Act of 2001 will not receive annual cost-of-living adjustments until their annuity amount is exceeded by the amount that would have been paid under prior law, counting all interim cost-of-living increases otherwise payable. Some 49% of the widow(er)s on the RRB’s rolls are being paid under the 2001 law.

If a Railroad Retirement or survivor annuitant also receives a Social Security or other government benefit, such as a public service pension, any cost-of-living increase in that benefit will offset the increased Tier I benefit. However, Tier II cost-of-living increases are not reduced by increases in other government benefits. If a widow(er) whose annuity is being paid under the 2001 law is also entitled to an increased government benefit, her or his Railroad Retirement survivor annuity may decrease.

In late December the RRB will mail notices to all annuitants providing a breakdown of the annuity rates payable to them in January 2023.

While railroad employees with less than 30 years of service may retire at age 62, their railroad retirement benefits are subject to early retirement (“age”) reductions if they retire before attaining their full retirement age.

The following questions and answers explain how full retirement age is determined, and how age reductions are applied to railroad retirement annuities.

1. How is full retirement age for a railroad employee with less than 30 years of service determined?

Full retirement age – the earliest age at which someone can begin receiving railroad retirement benefits that are not reduced for early retirement – is determined by the year a person was born. It has gradually increased since the year 2000, as a result of amendments to the Social Security Act which impacted railroad retirement annuitants and social security beneficiaries. Full retirement age for a railroad employee with less than 30 years of service is age 66 for those born in 1943 through 1954, and gradually increases to age 67 for those born in 1960, or later. (A chart listing employee birth years and the corresponding full retirement age is included in the answer to Question 2.)

2. Does the increase in full retirement age affect the computation of benefits reduced for early retirement?

Yes. The early retirement annuity reduction percentages applied to annuities awarded before full retirement age have increased. For employees retiring between age 62 and full retirement age with less than 30 years of service, the maximum reduction is 30% in 2022. Prior to 2000, the maximum reduction was 20%.

Age reduction percentages are applied separately to the tier I and tier II benefits of a railroad retirement annuity. The age reduction percentage is computed using the following formula: 1/180 for each of the first 36 months the employee is under full retirement age when his or her annuity begins, and 1/240 for each additional month (if any). This has resulted in the gradual increase in the annuity reduction percentage at age 62 to 30% for an employee, now that the full retirement age of age 67 is in effect. (See chart below.) However, if an employee had creditable railroad service before August 12, 1983, the retirement age for tier II purposes is age 65, and the tier II benefit will not be reduced beyond 20%.

The following chart shows the gradual increase in full retirement age and the corresponding increase in the age reduction percentages applied to the applicable employee annuities.

Employee Retires with Less than 30 Years of Service

Year of Birth*

Full Retirement Age**

Annuity Reduction at Age 62

1937 or earlier

65

20.00%

1938

65 and 2 months

20.833%

1939

65 and 4 months

21.667%

1940

65 and 6 months

22.50%

1941

65 and 8 months

23.333%

1942

65 and 10 months

24.167%

1943 through 1954

66

25.00%

1955

66 and 2 months

25.833%

1956

66 and 4 months

26.667%

1957

66 and 6 months

27.50%

1958

66 and 8 months

28.333%

1959

66 and 10 months

29.167%

1960 or later

67

30.00%

* A person attains a given age the day before his or her birthday. Consequently, someone born on January 1 is considered to have attained his or her given age on December 31 of the previous year. ** If an employee has less than 10 years of railroad service and is already entitled to an age-reduced social security benefit, the tier I reduction is based on the reduction applicable on the beginning date of the social security benefit, even if the employee is already of full retirement age on the beginning date of the railroad retirement annuity.

3. What are some examples of how age reductions are applied to the annuities of employees with less than 30 years of service who retire before attaining full retirement age?

Consider an employee who was born on March 2, 1960, and retired in 2022 at the age of 62. Assume this employee was eligible for monthly tier I and tier II benefits, before age reductions, of $1,800 and $1,200, respectively, for a total monthly annuity of $3,000.

Upon retirement at age 62, the employee’s tier I benefit and tier II benefit was reduced by 30.00%, the maximum age reduction applicable in 2022. This yielded a tier I amount of $1,260 and a tier II amount of $840, for a total monthly annuity of $2,100. However, if the employee had railroad service before August 12, 1983, the tier II amount would be subject to a maximum reduction of only 20%, providing a tier II amount of $960, and a total monthly annuity of $2,220.

As a second example, if the same employee had been born on March 2, 1959, and retired in 2022 at the age of 63, the employee’s tier I benefit and tier II benefit would be reduced by 24.167%. This would yield a tier I amount of $1,364.99 and a tier II amount of $910, for a total monthly annuity of $2,274.99. However, if the employee had railroad service before August 12, 1983, the tier II amount would be subject to a maximum reduction of only 20%, providing a tier II amount of $960, and a total monthly annuity of $2,324.99.

4. How are railroad retirement spouse benefits affected by these requirements?

If an employee retiring with less than 30 years of service is age 62, the employee’s spouse is also eligible for an annuity the first full month the spouse is age 62. However, early retirement reductions are applied to the spouse annuity if the spouse retires prior to her or his full retirement age.

Beginning in 2000, full retirement age for a spouse gradually began to rise to age 67, just as for an employee, depending on the spouse’s year of birth. While reduced spouse benefits are still payable at age 62, the maximum age reduction is 35% in 2022.

As with employee annuities, age reduction percentages are applied separately to the tier I and tier II benefits of a spouse annuity. However, the tier I reduction is 1/144 for each of the first 36 months the spouse is under full retirement age when her or his annuity begins, and 1/240 for each additional month (if any). This has resulted in a gradual increase in the annuity reduction percentage at age 62 to 35% for a spouse, now that the age 67 retirement age is in effect. (See chart below.) However, if an employee had any creditable railroad service prior to August 12, 1983, the spouse retirement age for tier II purposes is age 65 and the maximum age reduction percentage applied to tier II would only be 25%. Age reductions are not applied to spouse annuities based on the spouse’s caring for the employee’s child.

The following chart shows the gradual increase in full retirement age and the corresponding increase in the age reduction percentages applied to the applicable spouse annuities.

Spouse Age Reductions

Year of Birth*

Full Retirement Age**

Annuity Reduction at Age 62

1937 or earlier

65

25.00%

1938

65 and 2 months

25.833%

1939

65 and 4 months

26.667%

1940

65 and 6 months

27.50%

1941

65 and 8 months

28.333%

1942

65 and 10 months

29.167%

1943 through 1954

66

30.00%

1955

66 and 2 months

30.833%

1956

66 and 4 months

31.667%

1957

66 and 6 months

32.50%

1958

66 and 8 months

33.333%

1959

66 and 10 months

34.167%

1960 or later

67

35.00%

* A person attains a given age the day before her or his birthday. Consequently, someone born on January 1 is considered to have attained her or his given age on December 31 of the previous year. ** If the employee has less than 10 years of railroad service and the spouse is already entitled to an age-reduced social security benefit, the age reduction in her or his tier I will be based on the age reduction applicable on the beginning date of the spouse’s social security benefit, even if the spouse is already of full retirement age on the beginning date of her or his railroad retirement annuity.

5. What are some examples of how age reductions are applied to the annuities of the spouses of employees with less than 30 years of service whose spouses retire before full retirement age?

Consider the spouse of a railroader with less than 30 years of service, none of it prior to August 12, 1983, who was born on April 2, 1960, and is retiring in 2022 at age 62, with monthly tier I and tier II benefits, before any reductions for age, of $700 and $300, respectively, for a total monthly benefit of $1,000.

Upon retirement at age 62, the spouse’s tier I benefit and tier II benefit would be reduced by 35.00%, the maximum age reduction applicable in 2022. This would yield a tier I amount of $455 and a tier II amount of $195 for a total monthly annuity of $650. However, if the employee had any rail service before August 12, 1983, the tier II benefit would be subject to a maximum reduction of only 25%, providing a tier II amount of $225, and a total monthly annuity of $680.

As a second example, if the same spouse had been born on April 2, 1959, and retires in 2022 at age 63, the spouse’s tier I benefit and tier II benefit would be reduced by 29.167%. This would yield a tier I amount of $495.83 and a tier II amount of $212.50, for a total monthly annuity of $708.33. However, if the employee had any rail service before August 12, 1983, the tier II benefit would be subject to a maximum reduction of only 25%, providing a tier II amount of $225, and a total monthly annuity of $720.83.

6. Are age reductions applied to employee disability annuities?

Employee annuities based on disability are not subject to age reductions except for employees with less than 10 years of railroad service, but who have five years of service after 1995. Such employees may qualify for a tier I benefit before retirement age based on total disability, but only if they have a disability insured status (also called a “disability freeze”) under Social Security Act rules, counting both railroad retirement and social security-covered earnings. Unlike with a 10-year employee, a tier II benefit is not payable in these disability cases until the employee attains age 62. And, the employee’s tier II benefit will be reduced for early retirement in the same manner as the tier II benefit of an employee who retired at age 62 with less than 30 years of service.

7. Do these changes to full retirement age affect survivor benefits?

Yes. The eligibility age for a full widow(er)’s annuity has gradually risen, and is age 67 for those born in 1962, or later. A widow(er), surviving divorced spouse or remarried widow(er) whose annuity begins at full retirement age or later will generally receive an annuity unreduced for early retirement. (However, if the deceased employee received an annuity that was reduced for early retirement, a reduction would be applied to the tier I amount payable to his or her widow(er), surviving divorced spouse or remarried widow(er).) For widow(ers) who retire before attaining their full retirement age, the maximum age reduction percentages will vary, depending on the widow(er)’s date of birth, and is 20.36% for those born in 1962, or later. These age reductions apply to both tier I and tier II. For a surviving divorced spouse or remarried widow(er), the maximum age reduction is 28.5%. For a disabled widow(er), disabled surviving divorced spouse or disabled remarried widow(er), the maximum reduction is also 28.5%, even if the annuity begins at age 50.

8. Does the increase in full retirement age affect the age at which a person becomes eligible for Medicare benefits?

No. Although the age requirements for some unreduced railroad retirement benefits have risen just like the social security requirements, railroad retirement beneficiaries are still eligible for Medicare at age 65.

9. Do these increases in full retirement age also apply to the earnings limitations and work deductions governing benefit payments to annuitants who work after retirement?

Like social security benefits, railroad retirement tier I benefits paid to employees and spouses, and tier I and tier II benefits paid to survivors, are subject to deductions if an annuitant’s earnings exceed certain exempt amounts. These earnings limitations and work deductions apply to all age and service annuitants and spouses under full retirement age regardless of the employee’s years of service. Although employees retiring at age 60 with 30 years of service have no age reduction, these earnings limitations and work deductions still apply until they reach their full retirement age, which, like other employees, is determined by the year they were born. These earnings limitations also apply to survivor annuitants, with the exception of disabled widow(er)s under age 60 and disabled children.

Likewise, while special earnings restrictions apply to employees entitled to disability annuities, these disability earnings restrictions cease upon a disabled employee annuitant’s attainment of full retirement age. This transition is effective no earlier than full retirement age even if the annuitant had 30 years of railroad service.

The additional deductions applied to the annuities of retired employees and spouses who work for their last pre-retirement nonrailroad employer continue to apply after the attainment of full retirement age.

10. How can individuals get more information about railroad retirement age reductions?

Individuals with questions about railroad retirement age reductions can send a secure message to their local RRB office by accessing Field Office Locator at RRB.gov and clicking on the link at the bottom of their local office’s page. If a customer needs to talk to an RRB representative, they can call the agency’s toll-free number (1-877-772-5772) between the hours of 9 a.m. and 3 p.m. each weekday, except on federal holidays. However, customers are asked to be patient because of the increase in call volume due to the closure to the public of RRB offices during the COVID-19 pandemic.

In addition to the retirement annuities payable to railroad employees, the Railroad Retirement Act, like the Social Security Act, also provides annuities for some spouses of retired employees. Payment of a spouse annuity is made directly to the wife or husband of the employee. Divorced spouses may also qualify for benefits. The following questions and answers describe the benefits payable to spouses and the eligibility requirements. Information regarding divorced spouses begins with question eight. 1. How are Railroad Retirement spouse annuities computed? Regular Railroad Retirement annuities are computed under a two-tier formula. The Tier I portion of an employee’s annuity is based on both Railroad Retirement credits and any Social Security credits that the employee earned. Computed using Social Security benefit formulas, an employee’s Tier I benefit approximates the Social Security benefit that would be payable if all of the employee’s work were performed under the Social Security Act. The Tier II portion of the employee’s annuity is based on Railroad Retirement credits only, and may be compared to the retirement benefits paid over and above Social Security benefits to workers in other industries. The spouse annuity formula is based on percentages of the employee’s Tier I and Tier II amounts. The first tier of a spouse annuity, before any applicable reductions, is 50% of the railroad employee’s unreduced Tier I amount. The second tier amount, before any reductions, is 45% of the employee’s unreduced Tier II amount. 2. How does a Railroad Retirement spouse annuity compare to a Social Security spouse benefit? The average annuity awarded to spouses in fiscal year 2020, excluding divorced spouses, was $1,130 a month, while the average monthly Social Security spouse benefit was about $744. Annuities awarded in fiscal year 2020 to the spouses of employees who were of full retirement age or over and who retired directly from the rail industry with at least 25 years of service averaged $1,410 a month, and the average award to the spouses of employees retiring at age 60 or over with at least 30 years of service was $1,602 a month. 3. What are the age requirements for a Railroad Retirement spouse annuity? The age requirements for a spouse annuity depend on the employee’s age, date of retirement and years of railroad service. If a retired employee with 30 or more years of service is age 60 or older, the employee’s spouse is eligible for an annuity the first full month the spouse is age 60. Certain early retirement reductions are applied if the employee first became eligible for an annuity July 1, 1984, or later and retired at ages 60 or 61 before 2002. If the employee was awarded a disability annuity, has attained age 60, and has 30 years of service, the spouse can receive an unreduced annuity the first full month she or he is age 60, regardless of whether the employee annuity began before or after 2002, as long as the spouse’s annuity beginning date is after 2001. If a retired employee with less than 30 years of service is age 62 or older, the employee’s spouse is eligible for an annuity the first full month the spouse is age 62. Early retirement reductions are applied to the spouse annuity if the spouse retires prior to full retirement age. The full retirement age for a spouse is gradually rising to age 67, just as for an employee, depending on the year of birth. Reduced benefits are still payable at age 62, but the maximum reduction will be 35% rather than 25% by the year 2022. However, the Tier II portion of a spouse annuity will not be reduced beyond 25% if the employee had any creditable railroad service before August 12, 1983. 4. What if the spouse is caring for a child of the retired employee? A spouse of an employee who is receiving an age and service annuity (or a spouse of a disability annuitant who is otherwise eligible for an age and service annuity) is eligible for a spouse annuity at any age if caring for the employee’s unmarried child, and the child is under age 18 or a disabled child of any age who became disabled before age 22. 5. What are some of the other general eligibility requirements for a Railroad Retirement spouse annuity? The employee must have been married to the spouse for at least one year, unless the spouse is the natural parent of their child, or the spouse was eligible or potentially eligible for a Railroad Retirement widow(er)’s, parent’s or disabled child’s annuity in the month before marrying the employee or the spouse was previously married to the employee and received a spouse annuity. 6. Can the same-sex spouse of a railroad employee file for a Railroad Retirement spouse annuity? Yes, if the same-sex spouse meets current spouse annuity eligibility requirements and follows current application procedures. 7. Are spouse annuities subject to offset for the receipt of other benefits? Yes. The Tier I portion of a spouse annuity is reduced for any Social Security entitlement, regardless of whether the Social Security benefit is based on the spouse’s own earnings, the employee’s earnings or the earnings of another person. This reduction follows principles of Social Security law which, in effect, limit payment to the higher of any two or more benefits payable to an individual at one time. The Tier I portion of a spouse annuity may also be reduced for receipt of any federal, state or local government pension separately payable to the spouse based on the spouse’s own earnings. The reduction generally does not apply if the employment on which the public service pension is based was covered under the Social Security Act throughout the last 60 months of public employment. Most military service pensions and payments from the Department of Veterans Affairs will not cause a reduction. Pensions paid by a foreign government or interstate instrumentality will not cause a reduction. For spouses subject to a public service pension reduction, the Tier I reduction is equal to 2/3 of the amount of the public service pension. In addition, there may be a reduction in the employee’s Tier I amount for receipt of a public pension based, in part or in whole, on employment not covered by Social Security or Railroad Retirement after 1956. If the employee’s Tier I benefit is offset for a non-covered service pension, the spouse Tier I amount is 50% of the employee’s Tier I amount after the offset. The spouse Tier I portion may also be reduced if the employee is under age 65 and is receiving a disability annuity as well as worker’s compensation or public disability benefits. While these offsets can reduce or even completely wipe out the Tier I benefit otherwise payable to a spouse, they do not affect the Tier II benefit potentially payable to that spouse. 8. How do the eligibility requirements and benefits differ for a divorced spouse? A divorced spouse annuity may be payable to the divorced wife or husband of a retired employee if their marriage lasted for at least 10 consecutive years, both have attained age 62 for a full month, and the divorced spouse is not currently married. A divorced spouse can receive an annuity even if the employee has not retired, provided they have been divorced for a period of not less than two years, the employee and former spouse are at least age 62, and the employee is fully insured under the Social Security Act using combined railroad and Social Security earnings. Early retirement reductions are applied to the divorced spouse annuity if the divorced spouse retires prior to full retirement age. Full retirement age for a divorced spouse is gradually rising to age 67, depending on the year of birth. A divorced spouse is also eligible for an annuity at any age if caring for the employee’s unmarried child, and the child is under age 18, or a disabled child of any age who became disabled before age 22, if the employee is deceased. Unlike a regular spouse annuity, the divorced spouse annuity is computed under the single-Tier I formula. The amount of a divorced spouse’s annuity is, in effect, equal to what Social Security would pay in the same situation (Tier I only) and therefore less than the amount of the spouse annuity otherwise payable (Tier I and Tier II). The average divorced spouse annuity awarded in fiscal year 2020 was $768. 9. Would the award of an annuity to a divorced spouse affect the monthly annuity rate payable to a retired employee and/or the current spouse? No. If a divorced spouse becomes entitled to an annuity based on the employee’s railroad service, the award of the divorced spouse’s benefit would not affect the amount of the employee’s annuity, nor would it affect the amount of the Railroad Retirement annuity that may be payable to the current spouse. 10. What if an employee and spouse/divorced spouse are both railroad employees? If both started railroad employment after 1974, the amount of any spouse or divorced spouse annuity is reduced by the amount of the employee annuity to which the spouse is also entitled. If both the employee and spouse are qualified railroad employees and either had some railroad service before 1975, both can receive separate Railroad Retirement employee and spouse annuities, without a full dual benefit reduction. 11. Are Railroad Retirement annuities subject to garnishment or property settlements? Yes. Certain percentages of any Railroad Retirement annuity (employee, spouse, divorced spouse or survivor) may be subject to legal process (i.e., garnishment) to enforce an obligation for child support and/or alimony payments. Employee Tier II benefits and supplemental annuities are subject to court-ordered property divisions in proceedings related to divorce, annulment or legal separation. (Tier I benefits are not subject to property division.) A court-ordered property division payment may be paid even if the employee is not entitled to an annuity provided that the employee has 10 years of railroad service or five years after 1995 and both the employee and former spouse are at least age 62. 12. How can a person get more information about Railroad Retirement spouse and divorced spouse annuities? Individuals with questions about Railroad Retirement spouse and divorced spouse annuities can send a secure message to their local RRB office by accessing Field Office Locator at RRB.gov and clicking on the link at the bottom of their local office’s page. If a customer needs to talk to an RRB representative, they can call the agency’s toll-free number (1-877-772-5772) between the hours of 9 a.m. and 3 p.m. each weekday, except Federal holidays. However, customers are asked to be patient because of the increase in call volume due to the closure to the public of RRB offices during the COVID-19 pandemic.

Railroad Retirement benefits are based on months of service and earnings credits. Earnings are creditable, up to certain annual maximums, on the amount of compensation subject to Railroad Retirement taxes. Credit for a month of railroad service is earned for every month in which an employee had some compensated service covered by the Railroad Retirement Act. (Local lodge compensation is disregarded for any calendar month in which it is less than $25. However, work by a local lodge or division secretary collecting insurance premiums, regardless of the amount of salary, is creditable railroad work.) Also, under certain circumstances, additional service months may be deemed in some cases where an employee does not actually work in every month of the year. The following questions and answers describe the conditions under which an employee may receive additional Railroad Retirement service month credits under the deeming provisions of the Railroad Retirement Act. 1. What requirements must be met before additional service months can be deemed? A service month can be deemed if an employee has less than 12 service months reported in the year, has sufficient compensation reported and is in an “employment relation” with a covered railroad employer, or is an employee representative, during that month. (An employee representative is a labor official of a non-covered labor organization who represents employees covered under the acts administered by the Railroad Retirement Board.) For this purpose, an “employment relation” generally exists for an employee on an approved leave of absence (for example, furlough, sick leave, suspension, etc.). An “employment relation” is severed by retirement, resignation, relinquishing job rights in order to receive a separation allowance or termination. 2. How is credit for additional service months computed? For additional service months to be deemed, the employee’s compensation for the year, up to the annual Tier II maximum, must exceed an amount equal to 1/12 of the Tier II maximum multiplied by the number of service months actually worked. The excess amount is then divided by 1/12 of the Tier II maximum; the result, rounded up to the next whole number, equals the maximum number of months that may be deemed as service months for that year. Fewer months may be deemed, if an employment relation, as defined in Question 1, does not exist. 3. An employee works seven months in 2021 before being furloughed, but earns compensation of $108,000. How many deemed service months could be credited to the employee? The employee could be credited with five additional service months. One-twelfth of the 2021 $106,200 Tier II maximum ($8,850) times the employee’s actual service months (seven) equals $61,950. The employee’s compensation in excess of $61,950 up to the $106,200 maximum is $44,250, which divided by $8,850 equals five. Therefore, five deemed service months could be added to the seven months actually worked and the employee would receive credit for 12 service months in 2021. 4. Another employee works for seven months in 2021 and earns compensation of $85,200. How many deemed service months could be credited to this employee? In this case, the excess amount ($85,200 minus $61,950) is $23,250, which divided by $8,850 equals 2.627. After rounding, this employee could receive credit for three deemed service months and be credited with a total of 10 months of service in 2021. 5. Another employee works for eight months in 2021 before resigning on August 15, but earns compensation of $91,000. How many deemed service months could be credited to this employee? None. Since the employee resigned in August, there is no employment relationship for the remaining months and no additional service months may be deemed and credited. 6. Should an employee preparing to retire take deemed service months into account when designating the date his or her Railroad Retirement annuity begins? An employee may wish to consider credit for deemed service months in selecting an annuity beginning date. For instance, in some cases, a designated annuity beginning date that considers deemed service months could be used to establish basic eligibility for certain benefits, increase an annuity’s Tier II amount, or establish a current connection, as illustrated in Questions 7, 8 and 9, respectively. It should be noted that service months cannot be deemed after the annuity beginning date. 7. What would be an example of using deemed service months to establish benefit eligibility? An example would be an employee between the ages of 60 and 62 who might be able to use deemed service months to establish the 360 months of service needed to qualify for an unreduced age annuity prior to full retirement age. For instance, a 60-year-old employee last performed service on May 15, 2021, and received $61,800 in compensation in 2021. She is credited with 358 months of creditable railroad service through May 2021. If the employee wishes to retire on age, she must wait until she is full retirement age, which ranges between 66 and 67 depending upon the employee’s year of birth, or age 62 if she is willing to accept an age-reduced annuity. She needs at least two additional months of service to establish eligibility for an unreduced annuity prior to full retirement age. The employee’s excess amount ($61,800 minus $44,250) is $17,550, which divided by $8,850 equals 1.983. Therefore, two deemed service months could be added to the five months actually worked and the employee would receive credit for seven service months in 2021 for a total of 360 service months, allowing her to receive an unreduced annuity beginning July 2, 2021. 8. How could deemed service months be used to increase an employee’s Tier II amount? An employee worked in the first five months of 2021 and received compensation of $59,500. He does not relinquish his rights until July 2, 2021, and applies for an annuity to begin on that date. The excess amount ($59,500 minus $44,250) is $15,250, which divided by $8,850 equals 1.723, which yields two deemed service months for a total of seven service months in 2021. Had the employee relinquished his rights and applied for an annuity to begin on July 1, he would have been given credit for only six service months. The employee received the maximum compensation in all of the last five years and had 360 months of service through 2020. The additional service and compensation increases his Tier II from $1,726.75 to $1,746.92. However, delaying the annuity beginning date past the second day of the month after the date last worked solely to increase the Tier II amount would not generally be to the employee’s advantage. 9. Can deemed service months help an employee establish a current connection? Yes. For example, an employee left the railroad industry in 2002 and engaged in employment covered by the Social Security Act. In August 2020, she returned to railroad employment and worked through June 28, 2021. She received compensation of $53,650 in 2021. She does not relinquish her rights until July 2, 2021, and applies for an annuity to begin on July 2, 2021. In this case, the excess amount ($53,650 minus $53,100) is $550, which divided by $8,850 equals 0.0621, which yields one deemed service month. Consequently, the employee is given credit for seven service months in 2021. With five months of service in 2020 and seven months in 2021, the employee establishes a current connection. Had she designated the earliest annuity beginning date permitted by law, she would not have met the 12-in-30-month requirement for a current connection. (An employee who worked for a railroad in at least 12 months in the 30 months immediately preceding the month his or her Railroad Retirement annuity begins will meet the current connection requirement for a supplemental annuity, occupational disability annuity or survivor benefits.) 10. Can an employee ever receive credit for more than 12 service months in any calendar year? No. Twelve service months are the maximum that can be credited for any calendar year. 11. Where can an employee get more information on how deemed service months could affect his or her annuity? Employees with questions about deemed service months can send a secure message to their local RRB office by accessing Field Office Locator at RRB.gov and clicking on the link at the bottom of their local office’s page. If a customer needs to talk to an RRB employee, they can call the agency’s toll-free number (1-877-772-5772). However, customers are asked to be patient because of the increase in call volume due to the closure to the public of RRB offices during the COVID-19 pandemic.

The Railroad Retirement Board (RRB) administers the Railroad Unemployment Insurance Act (RUIA), which provides two kinds of benefits for qualified railroaders: unemployment benefits for those who become unemployed but are ready, willing and able to work; and sickness benefits for those who are unable to work because of sickness or injury. Sickness benefits are also payable to female rail workers for periods of time when they are unable to work because of health conditions related to pregnancy, miscarriage or childbirth. A new benefit year begins each July 1.

The following questions and answers describe these benefits, their eligibility requirements and how to claim them. At the time this news release was issued, unemployment and sickness benefit flexibilities were in place due to the COVID-19 pandemic. Because these flexibilities are temporaryand may change, they are not covered in this release. Visit RRB.gov/coronavirus for up-to-date information.

1. What are the eligibility requirements for railroad unemployment and sickness benefits in July 2021?

To qualify for normal railroad unemployment or sickness benefits, an employee must have had railroad earnings of at least $4,137.50 in calendar year 2020, counting no more than $1,655 for any one month. Those who were first employed in the rail industry in 2020 must also have at least five months of creditable railroad service in 2020.

Under certain conditions, employees who do not qualify on the basis of their 2020 earnings may still be able to receive benefits in the new benefit year. Employees with at least 10 years of service (120 or more months of service) who received normal benefits in the benefit year ending June 30, 2021, may be eligible for extended benefits. Employees with at least 10 years of service (120 or more months of service) might qualify for accelerated benefits if they have railroad earnings of at least $4,275 in 2021, not counting earnings of more than $1,710 in any one month.

In order to qualify for extended unemployment benefits, a claimant must not have voluntarily quit work without good cause and not have voluntarily retired. To qualify for extended sickness benefits, a claimant must not have voluntarily retired and must be under age 65.

To be eligible for accelerated benefits, a claimant must have 14 or more consecutive days of unemployment or sickness; not have voluntarily retired or, if claiming unemployment benefits, quit work without good cause; and, when claiming sickness benefits, be under age 65.

2. What is the daily benefit rate payable in the new benefit year beginning July 1, 2021?

Almost all employees will qualify for the maximum daily benefit rate of $82. Benefits are generally payable for the number of days of unemployment or sickness over four in 14-day claim periods, which yields $820 for each two full weeks of unemployment or sickness. Sickness benefits payable for the first 6 months after the month the employee last worked are subject to Tier I Railroad Retirement payroll taxes, unless benefits are being paid for an on-the-job injury.

Claimants should be aware that as a result of a sequestration order under the Budget Control Act of 2011, the RRB will reduce unemployment and sickness benefits by 5.7% through September 30, 2021. Consequently, the total maximum amount payable in a 2-week period covering 10 days of unemployment or sickness will be $773.26. The maximum amount payable for sickness benefits subject to Tier I payroll taxes of 7.65% will be $714.11 over two weeks. Future reductions, should they occur, will be calculated based on applicable law.

(The temporary benefits created under the Coronavirus Aid, Relief, and Economic Security Act, Continued Assistance to Rail Workers Act of 2020 (CARWA), and American Rescue Plan Act of 2021 are not subject to sequestration. Under CARWA, beginning January 3, 2021, all benefits under the RUIA (including normal unemployment and sickness benefits as well as normal extended unemployment and sickness benefits) will be exempt from sequestration until 30 days after the Presidential declaration of a national emergency concerning COVID-19 terminates. The RRB will publish updated information regarding the status of the sequestration of RUIA benefits when the end date of the Presidential declaration of a national emergency is known.)

3. How long are these benefits payable?

Normal unemployment or sickness benefits are each payable for up to 130 days (26 weeks) in a benefit year. The total amount of each kind of benefit which may be paid in the new benefit year cannot exceed the employee’s railroad earnings in calendar year 2020, counting earnings up to $2,138 per month.

If normal benefits are exhausted, extended benefits are payable for up to 65 days (during seven consecutive 14-day claim periods) to employees with at least 10 years of service (120 or more cumulative service months).

4. What is the waiting period requirement for unemployment and sickness benefits?

There is a seven-day waiting period requirement, prior to any benefits becoming payable under the RUIA. During the first 14-day claim period, benefits are payable for every day claimed in excess of seven days. Subsequent claims are paid for the number of days of unemployment or sickness over four in each 14-day registration period. Initial sickness claims must also begin with four consecutive days of sickness. If an employee has at least five days of unemployment or five days of sickness in a 14-day period, he or she should still file for benefits in order to satisfy the waiting period for the current benefit year. Separate waiting periods are required for unemployment and sickness benefits. However, only one seven-day waiting period is generally required during any period of continuing unemployment or sickness, even if that period continues into a subsequent benefit year.

5. Are there special waiting period requirements if unemployment is due to a strike?

If a worker is unemployed because of a strike conducted in accordance with the Railway Labor Act, benefits are not payable for days of unemployment during the first 14 days of the strike, but benefits are payable during subsequent 14-day periods.

If a strike is in violation of the Railway Labor Act, unemployment benefits are not payable to employees participating in the strike. However, employees not among those participating in such an illegal strike, but who are unemployed on account of the strike, may receive benefits after the first two weeks of the strike.

While a benefit year waiting period cannot count toward a strike waiting period, the 14-day strike waiting period may count as the benefit year waiting period if a worker subsequently becomes unemployed for reasons other than a strike later in the benefit year.

6. Can employees in train and engine service receive unemployment benefits for days when they are standing by or laying over between scheduled runs?

No, not if they are standing by or laying over between regularly assigned trips or they missed a turn in pool service.

7. Can extra-board employees receive unemployment benefits between jobs?

Yes, but only if the miles and/or hours they actually worked were less than the equivalent of normal full-time work in their class of service during the 14-day claim period. Entitlement to benefits would also depend on the employee’s earnings.

8. How would an employee’s earnings in a claim period affect his or her eligibility for unemployment benefits?

If a claimant’s earnings for days worked, and/or days of vacation, paid leave or other leave in a 14-day registration period are more than a certain indexed amount, no benefits are payable for any days of unemployment in that period. That registration period, however, can be used to satisfy the waiting period.

Earnings include pay from railroad and non-railroad work, as well as part-time work and self-employment. Earnings also include pay that an employee would have earned except for failure to mark up or report for duty on time, or because he or she missed a turn in pool service or was otherwise not ready or willing to work. For the benefit year that begins July 2021, earnings of $1,655 or more in a claim period will disqualify a claim for unemployment benefits, even if there are more than 4 days of unemployment claimed. This amount corresponds to the base year monthly compensation amount used in determining eligibility for benefits in each year. Also, even if an earnings test applies on the first claim in a benefit year, this will not prevent the first claim from satisfying the waiting period in a benefit year.

Earnings of $15 or less per day from work which is substantially less than full-time and not inconsistent with the holding of normal full-time employment may be considered subsidiary remuneration and may not prevent payment of any days in a claim. However, a claimant must report all full and part-time work on each claim, regardless of the amount of earnings, so the RRB can determine if the work affects benefits.

9. How does a person apply for and claim unemployment benefits?

Employees can apply for and claim unemployment benefits online or by mail. Individuals who have established an account through myRRB at RRB.gov can log in and file their applications and their biweekly claims online. Employees who need to create an account should visit RRB.gov/myRRB and click on the button labeled Sign in with login.gov. Employees are encouraged to establish their accounts while still working to expedite the filing process for future unemployment benefits, and for access to other online services.

To apply by mail, claimants must obtain an Application for Unemployment Benefits (Form UI-1) from RRB.gov, their labor organization or railroad employer. The completed application should be mailed to the local RRB office as soon as possible and must be filed within 30 days from the date the claimant became unemployed, or the first day for which he or she wishes to claim benefits. Benefits may be lost if the application is filed late. Claimants filing a late unemployment application or claim should include a signed statement explaining why they are unable to meet the required time frame.

Persons can find the address of the RRB office serving his or her area by visiting RRB.gov and clicking on Field Office Locator, or by calling the agency toll-free at 1-877-772-5772 and selecting the appropriate option from the automated menu.

The local RRB field office reviews the completed application, whether it was submitted online or by mail, and notifies the claimant’s current railroad employer, and base-year employer, if different. The employer has the right to provide information about the benefit application.

After processing the application, biweekly claim forms are provided to the claimant for as long as he or she remains unemployed and eligible for benefits. If a claimant filed an online application, his or her claim forms are only made available online. If a claimant filed a paper application, his or her first claim form is both available online and mailed to him or her. If the claimant returns the paper claim, future claims will be mailed to him or her. If the claimant files the claim online, all subsequent claim forms will only be made available online, and will no longer be mailed. Claimants mustnot file both an online and a paper claim form for the same period(s). Claim forms should be signed and sent (online or by mail) on or after the last day of the claim. The completed claim must be received by the RRB within 15 days of the end of the claim period, or within 15 days of the date the claim form was made available online or mailed to the claimant, whichever is later.

Only one application needs to be filed during a benefit year, even if a claimant becomes unemployed more than once. However, in the case of multiple claim periods, a claimant must request a claim form from the RRB within 30 days of the first day for which he or she wants to resume claiming benefits. These claim forms may then be filed online or by mail.

10. How does a person apply for and claim sickness benefits?

An Application for Sickness Benefits (Form SI-1a) can be obtained from RRB.gov, a railroad labor organization, or a railroad employer. Applications for sickness benefits must be submitted to the agency by mail. However, subsequent claims may be mailed, or completed online by employees who have established a myRRB account at RRB.gov.

An application including a doctor’s Statement of Sickness (Form SI-1b – included with form SI-1a) is required at the beginning of each period of continuing sickness for which benefits are claimed. Claimants should make a special effort to have the doctor’s statement of sickness completed promptly since claims cannot be paid without it.

The RRB suggests that employees keep an application for sickness benefits on hand, and that family members know where the form is kept and how to use it. If an employee becomes unable to work because of sickness or injury, the employee should complete the application and have his or her doctor complete the attached statement of sickness. If a claimant receives sickness benefits for an injury or illness for which he or she is paid damages, it is important to be aware that the RRB is entitled to reimbursement of either the amount of the benefits paid for the injury or illness or the net amount of the settlement, after deducting the claimant’s gross medical, hospital and legal expenses, whichever is less.

After completion, the forms should be mailed to the RRB’s headquarters in Chicago within 10 days from when the employee became sick or injured. However, applications received after 10 days but within 30 days of the first day for which an employee wishes to claim benefits are generally considered timely filed if there is a good reason for the delay. (Employees cannot currently file their sickness applications online.) Upon receipt, the RRB will process the application and determine if the employee is eligible for sickness benefits.

After processing the application and statement of sickness, the RRB makes the first biweekly claim form available online (for employees with myRRB accounts) and mails a paper form to the employee as long as he or she is eligible for benefits and remains unable to work due to illness or injury. Those choosing to file the paper claim received by mail should return the completed form to RRB headquarters for processing. If the claimant returns the paper claim, future claims will be mailed to him or her. If the claimant files the claim online, all subsequent claim forms will only be made available online, and will no longer be mailed. Claimants must not file both online and paper claim forms for the same claim period(s). Employees who need to create a myRRB account should visit RRB.gov/myRRB and click on the button labeled Sign in with login.gov.

Completed claim forms must be received at the RRB within 30 days of the last day of the claim period, or within 30 days of the date the claim form was made available online or mailed to the claimant, whichever is later. Benefits may be lost if an application or claim form is filed late. Claimants filing a late sickness application or claim form should include a signed statement explaining why they were unable to meet the required time frame.

Claimants are reminded that while claim forms for sickness benefits can be submitted online, applications for sickness benefits must be mailed to the RRB. Statements of sickness may be mailed with the sickness application or faxed directly from the doctor’s office to the RRB at 312-751-7185. Faxes must include a cover sheet from the doctor’s office. Also, in order to prevent a delay in processing applications or claims, employees are advised against sending any sickness benefit forms to the RRB in Chicago via certified mail.

11. Is a claimant’s employer notified each time a biweekly claim for unemployment or sickness benefits is filed?

The RUIA requires the RRB to notify the claimant’s base-year employer each time a claim for benefits is filed. That employer has the right to submit information relevant to the claim before the RRB makes an initial determination on the claim. Benefits may not be paid at this time but the employee will receive a notice and have the right to appeal. In addition, if a claimant’s base-year employer is not his or her current employer, the claimant’s current employer is also notified. The RRB must also notify the claimant’s base-year employer each time benefits are paid to a claimant. The base-year employer may protest the decision to pay benefits. Such a protest does not prevent the timely payment of benefits. However, a claimant may be required to repay benefits if the employer’s protest is ultimately successful. The employer also has the right to appeal an unfavorable decision to the RRB’s Bureau of Hearings and Appeals.

The RRB also conducts checks with other Ffederal agencies and all 50 states, as well as the District of Columbia and Puerto Rico, to detect fraudulent benefit claims, and it checks with physicians to verify the accuracy of medical statements supporting sickness benefit claims.

12. How long does it take to receive payment?

Under the RRB’s Customer Service Plan, if a claimant files an application for unemployment or sickness benefits, the RRB will release a claim form or a denial letter within 10 days of receiving his or her application. If a claim for subsequent biweekly unemployment or sickness benefits is filed, the RRB will certify a payment or release a denial letter within 10 days of the date the RRB receives the claim form. If the claimant is entitled to benefits, his or her benefits will generally be paid within one week of that decision.

If a claimant does not receive a decision notice or payment within the specified time period, he or she may expect an explanation for the delay and an estimate of the time required to make a decision.

However, some claims for benefits may take longer to handle than others, especially if they are more complex, or if an RRB office has to get information from other people or organizations, or under special circumstances such as the current pandemic.

Claimants who think an RRB office made the wrong decision about their benefits have the right to ask for review and to appeal. They will be notified of these rights each time an unfavorable decision is made on their claims.

13. How are payments made?

Railroad unemployment and sickness insurance benefits are paid by direct deposit to an employee’s bank, savings and loan, credit union or other financial institution. New applicants for unemployment and sickness benefits will be asked to provide information needed for direct deposit enrollment.

14. How can claimants get more information on their railroad unemployment or sickness claims?

Claimants with myRRB accounts can view their individual railroad unemployment and sickness insurance account statement by using the View RUIA Account service. This statement displays the type and amount of the claimant’s last five benefit payments, the claim period for which the payments were made, and the dates that the payments were approved. Individuals can also confirm the RRB’s receipt of applications and claims.

In addition, claimants can call the agency toll-free at 1-877-772-5772 to access information about the status of unemployment and sickness claims or payments 24 hours a day, 7 days a week. Individuals with questions about unemployment or sickness benefits, or who need information about their specific claims and benefit payments, can send a secure e-mail to their local office by accessing the Field Office Locator at RRB.gov and clicking on the link at the bottom of their local office’s page. If a customer needs to talk to an RRB employee, they can call the agency’s toll-free number (1-877-772-5772). However, customers are asked to be patient because of the increase in call volume due to the closure to the public of RRB offices during the COVID-19 pandemic.

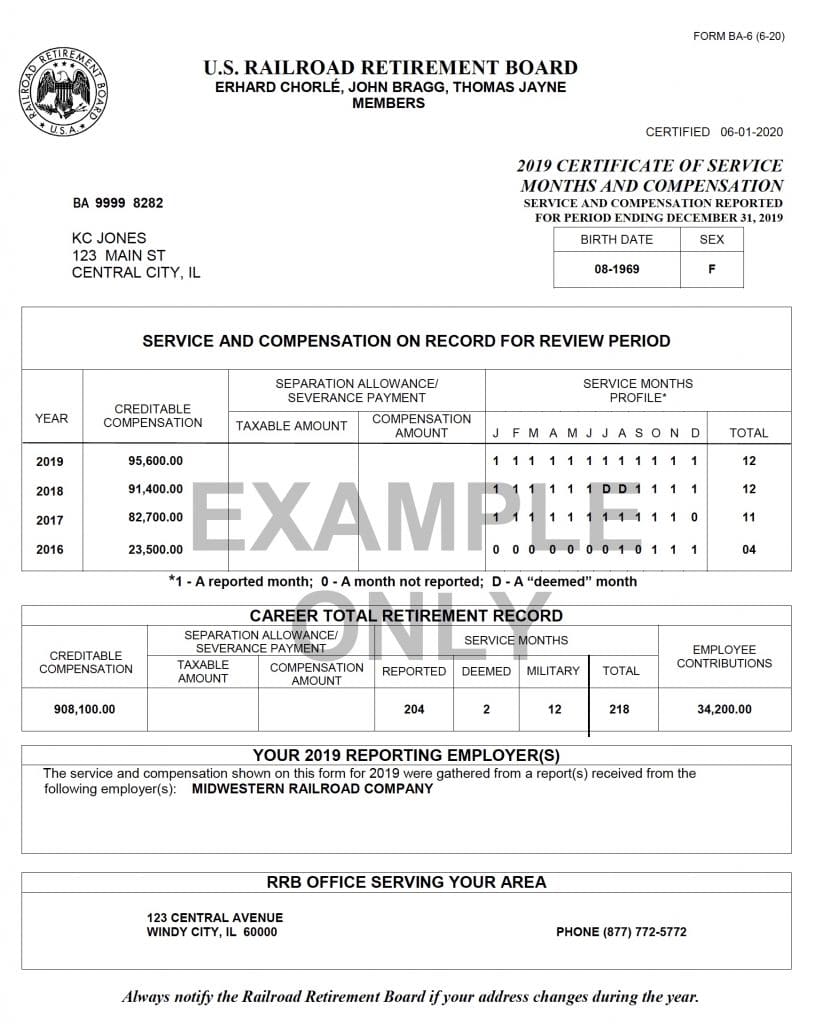

Brothers and Sisters, RRB Labor Member John Bragg It is hard to believe that 2020 is in the rearview mirror and we are already approaching the mid-point of 2021. The Railroad Retirement Board (RRB) is still operating in a remote capacity with field offices closed to the public. Hopefully, in the not too distant future, I will be writing to advise you of plans for getting back to normal operations. Today, however, I am writing to share a friendly reminder with you about action which every active employee should take on an annual basis – and may be of particular importance this year to some, in light of the unique work circumstances many encountered. Each year, on or before the last day of February, employers must report service and compensation for each employee who performed compensated service in the preceding calendar year. The RRB, in turn, credits the service and compensation records of individual employees based upon these reports and in June of every year, the RRB releases Form BA-6 to each employee for which compensated service for the preceding year was reported. The Form BA-6 contains the information recently reported for the preceding year, as well as the information reported for three preceding years. For example, the Forms BA-6 which will be released by the RRB in mid-June of 2021 will contain service and compensation reported for the years 2017 through 2020. Regardless of the amount earned, the amount of compensation shown on the Form BA-6 will always be limited by the maximum creditable Tier I compensation amount for the calendar year. For calendar years 2017 through 2020, the maximum amounts creditable are $127,200, $128,400, $132,900 and $137,700, respectively. In addition to showing the creditable compensation for the years 2017 through 2020, the Form BA-6 issued in mid-June of 2021 will show the months for which the employer reported railroad service for the employee during the years 2017-2020. It is critical that individual employees review their annual Forms BA-6 to make sure that all the information contained on the form is accurate. For example, in addition to validating the creditable compensation, it is important to check to see if the employer properly reported the months for which credit was given by the employer for a month of railroad service. Every month for which you believe you should have credit for railroad service should be coded with a “1”. If the code is “0”, you will not receive credit for any railroad service for that month. If the code is “D” then you will receive credit for railroad service pursuant to the rules governing the deeming of service months. Employees who received pay for time lost, especially as a result of arbitration proceedings, during the years 2017 through 2020 are reminded of the importance of checking their Forms BA-6. RRB regulations at 20 C.F.R. § 209.15(b) provide that compensation which is pay for time lost must be reported with respect to the year in which the time and compensation were lost. However, it is not uncommon for the individuals responsible for completing reports of service and compensation to be unfamiliar with how to report pay for time lost, or to lack awareness that the compensation they are reporting reflects pay for time lost. As a result, the compensation is mistakenly reported for the year paid AND the service months for which the time and compensation were lost are not credited as railroad service months. Situations where this is most likely to occur are arbitration decisions resulting in the employee being reinstated with all rights and benefits unimpaired and receiving compensation for lost time. REMEMBER: The law limits the period during which corrections to service and compensation records may be filed to four years from the date the report was due at the RRB, so it is very important for employees to request a correction within that period of time. Any railroad employee who thinks that the Form BA-6 contains an error should be certain to follow the directions on how to file with the RRB a protest of the information contained on the Form BA-6.