The chief actuary of the Railroad Retirement Board (RRB) said in his triennial report that the railroad retirement fund will remain solvent with no cash flow problems for nearly three decades, barring any unforeseen drops in rail worker employment over that time. The positive forecast led the reviewers to conclude that the RRB payroll tax structure should remain unchanged at present, yet they also warned that future job losses could jeopardize the system in years to come. “The long-term stability of the system, however, is not assured,” Chief Actuary Frank J. Buzzi and his staff wrote. “Under the current financing structure, actual levels of railroad employment and investment return over the coming years will determine whether additional corrective action is necessary.” Chief Actuary Frank Buzzi and his staff said in the report, submitted by RRB in mid-June to President Donald Trump, Vice President Michael Pence and Speaker of the House Paul Ryan, that cash flow for rail retirement appears stable until 2047. “The conclusion is that, barring a sudden, unanticipated, large drop in railroad employment of substantial investment losses, the railroad retirement system will experience no cash flow problems during the next 29 years.” Frank Buzzi and his staff wrote. The review assumed three scenarios for passenger and freight railroad employment from 2017 and the years after and projected the status of the system out to 2091.

Scenario 1 (optimistic): Average railroad employment starts at 223,000, with passenger employment steady at 48,000 workers and a constant annual decline in freight rail employment of 0.5 percent for 25 years at a reducing rate over the next 25 years and then remaining level thereafter.

Scenario 2 (moderate): Average railroad employment starts at 223,000, with passenger employment steady at 48,000 with a constant annual decline in freight rail employment of 2 percent for 25 years, at a reducing rate over the next 25 years, and remain level thereafter.

Scenario 3 (pessimistic): Average railroad employment starts at 223,000, with a decline of 500 workers per year in passenger employment until it stabilizes at 40,000; freight employment would decline at a constant annual rate of 3.5 percent for 25 years, then at a reducing rate over the next 25 years, and remain level thereafter.

Only in the third scenario, with the loss of 122,000 workers over the 29 years, did the railroad retirement system run into cash troubles in 2047. Held constant in the review were variables such as earnings (3.6 percent), cost-of-living increases (2.6 percent) and investment returns (7 percent). Also kept constant were non-economic factors such as mortality, disability, retirements and withdrawal. Follow this link to read a PDF of the complete report.

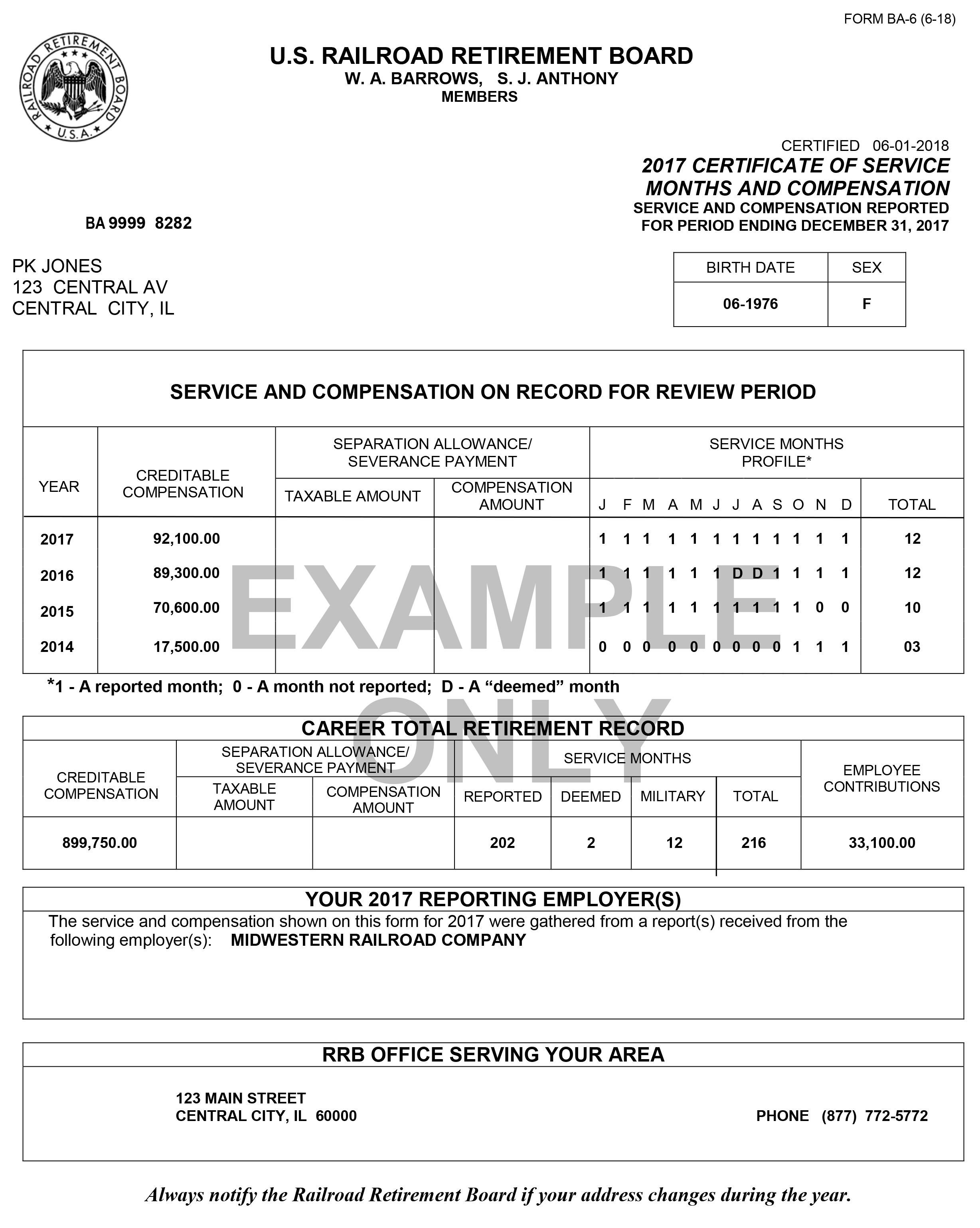

Each year, the U.S. Railroad Retirement Board (RRB) prepares a “Certificate of Service Months and Compensation” (Form BA-6) for every railroad employee with creditable railroad compensation in the previous calendar year. The RRB will mail the forms to employees during the first half of June. While every effort has been made to maintain current addresses for all active railroad employees, anyone with compensation reported in 2017 who has not received Form BA-6 by July 1, or needs a replacement, should contact an RRB field office by calling the agency toll-free at 1-877-772-5772.

Form BA-6 provides employees with a record of their railroad retirement service and compensation, and the information shown is used to determine whether an employee qualifies for benefits and the amount of those benefits. It is important that employees review their Form BA-6 to see whether their own records of service months and creditable compensation agree with the figures shown on the form.

In checking the 2017 compensation total, employees should be aware that only annual earnings up to $127,200 were creditable for railroad retirement purposes in that year, and that $127,200 is the maximum amount shown on the form. To assist employees in reviewing their service credits, the form also shows service credited on a month-by-month basis for 2016, 2015 and 2014, when the creditable compensation maximum was $118,500 for both 2016 and 2015, and $117,000 for 2014. The form also identifies the employer(s) reporting the employee’s 2017 service and compensation.

Besides the months of service reported by employers, Form BA-6 shows the number of any additional service months deemed by the RRB. Deemed service months may be credited under certain conditions for an employee who did not work in all 12 months of the year, but had creditable tier II earnings exceeding monthly prorations of the creditable tier II earnings maximum for the year. However, the total of reported and deemed service months may never exceed 12 in a calendar year, and no service months, reported or deemed, can be credited after retirement, severance, resignation, discharge or death.

The form also indicates the number of months of verified military service creditable as service under the Railroad Retirement Act, if the service was previously reported to the RRB. Employees are encouraged to submit proofs of age and/or military service in advance of their actual retirement. Filing these proofs with the RRB in advance will streamline the benefit application process and prevent payment delays.

For employees who received separation or severance payments, the section of the form designated “Taxable Amount” shows the amounts reported by employers of any separation allowance or severance payments that were subject to railroad retirement tier II taxes. This information is shown on the form because a lump sum, approximating part or all of the tier II taxes deducted from such payments made after 1984 which did not provide additional tier II credits, may be payable by the RRB upon retirement to qualified employees or to survivors if the employee dies before retirement. The amount of an allowance included in an employee’s regular compensation is shown under “Compensation Amount.”

Form BA-6 also shows, in the section designated “Employee Contributions,” the cumulative amount of tier II railroad retirement payroll taxes paid by the employee over and above tier I social security equivalent payroll taxes. While the RRB does not collect or maintain payroll tax information, the agency computes this amount from its compensation records in order to advise retired employees of their payroll tax contributions for Federal income tax purposes.

Employees should check their name, address, birth date and sex shown at the top of the form. If the form shows the birth date as 99-9999 and the gender code is “U” (for unknown), it means the RRB is verifying his or her social security number with the Social Security Administration. Otherwise, if the personal identifying information is incorrect or incomplete (generally a case where the employee’s surname has more than 10 letters and the form shows only the first 10 letters) or the address is not correct, the employee should contact an RRB field office. The field office can then correct the RRB’s records. This is important in order to prevent identity or security-related problems that could arise if the employee wants to use certain internet services available on the RRB’s website at www.rrb.gov.

Employees may view their railroad retirement service and compensation records; get annuity estimates; apply for or claim railroad unemployment benefits; claim sickness benefits and access their railroad unemployment insurance account statements through the RRB’s website. To use these online services, an employee must set up an RRB online account and obtain a password. Instructions for establishing an online account can be accessed via the “Benefit Online Services” link on the home page. For security purposes, first-time users must enter a Password Request Code (PRC). The agency automatically mails a PRC to any employee who files a paper application for unemployment or sickness benefits. If an individual has not received a PRC, they can request one by clicking the appropriate link on the “Benefit Online Services” page. They will then receive the PRC by mail at their home address in about 10 days.

Employees can also request that printouts of their individual railroad retirement records of service months and compensation be mailed to them. A PIN/Password is not required to use this service. It can be accessed by visiting www.rrb.gov, going to “Benefit Online Services” and then clicking on “No Login Required.”

If the employee’s name was incomplete on Form BA-6, and he or she has not yet contacted an RRB field office to correct it, the employee should enter his or her first and middle initials and his or her surname just as it appears on the Form BA-6 or a previously furnished printout of service and compensation, along with the other requested information, in order to submit an online request.

Any other discrepancies in Form BA-6 should be reported promptly in writing to:

Protest Unit-CESC U.S. Railroad Retirement Board 844 North Rush Street Chicago, Illinois 60611-1275

The employee must include his or her social security number in the letter. Form BA-6 also explains what other documentation and information should be provided. The law limits to four years the period during which corrections to service and compensation amounts can be made.

For most employees, the address of the RRB office serving their area is provided on the form along with the RRB’s nationwide toll-free number (1-877-772-5772). RRB field offices are open to the public from 9:00 a.m. to 3:30 p.m. on Monday, Tuesday, Thursday and Friday, and from 9 a.m. to noon on Wednesday, except on federal holidays.

WASHINGTON, D.C. – Congress passed and President Trump signed into law Friday a bipartisan spending agreement also known as the “omnibus” spending bill that provides a massive boost toward several of our union’s priorities, including transportation infrastructure projects, the Railroad Retirement Board and the National Mediation Board. With the growing demand by our nation’s leaders to address infrastructure needs, the omnibus provides a major boost to funding passenger rail and transit projects such as $1.9 billion for Amtrak, including $650 million for projects in the Northeast Corridor. This will provide much-needed funding for the Gateway Project that will double passenger train service between New York and New Jersey to reduce congestion while making repairs to tunnels and tracks that are long overdue. For our bus and transit members, the bill provides $2.6 billion to fund major transit capital investments, including heavy rail, commuter rail, light rail, streetcars and bus rapid transit projects nationwide. In addition, the Railroad Retirement Board received a $10 million boost that will allow the agency to phase out its decades-old hardware systems with modernized Information Technology services to provide and disburse benefits to our railroad retirees in a timely manner. Lastly, the omnibus provides the National Mediation Board with $13.8 million that includes the sustained $570,000 funding increase to address the arbitration backlog. “The SMART TD National Legislative Office continues to inform lawmakers about the importance of funding transit and passenger rail that are vital to our union membership and the nation’s transportation workforce at large. We will continue working to ensure that Congress addresses the full needs of our rail workers by increasing resources for the National Mediation Board and Railroad Retirement Board so that our members receive the services they earned and deserve,” SMART TD National Legislative Director John Risch said.

The U.S. Railroad Retirement Board (RRB) has announced that during the lapse in federal funding for certain government operations which began Jan. 20, ongoing benefit payments will continue and all RRB offices are expected to remain open.

RRB field offices, operating with reduced staffs, will continue to accept new claims for unemployment and sickness benefits, as well as new applications for retirement, survivor, and disability benefits. People receiving ongoing benefit payments are still obliged to report any events that would affect the payment of their benefits.

Individuals calling the RRB’s toll-free telephone number (1-877-772-5772) and having difficulty in reaching an agency representative are asked to be patient as offices are operating with a very limited staff.

The office of Walter Barrows, the labor member of the Railroad Retirement Board (RRB) announced changes to the board’s 2018 slate of informational meetings in a release distributed Wednesday. Rail union officials and any interested rail employees within five years of retirement and their spouses are able to register for combined informational conference/pre-retirement seminars this year at the following dates and locations: • March 23 in Roseville, Calif.; • May 11 in Altoona, Pa.; • Sept 21 in Bellevue, Wash.; • Nov. 16 in Houston; • Dec. 7 in Jacksonville, Fla. The RRB still plans separate conferences and seminars at additional locations across the country. The board will post a schedule in the future on the RRB’s website (www.rrb.gov). RRB field service managers will lead the combined programs and present the various railroad retirement benefits available to employees and their families and informational materials to attendees. The combined programs will close with a separate brief presentation spotlighting railroad unemployment and sickness benefits that will be conducted for those rail officials in attendance only. More details on the informational programs, including registration forms, dates and exact meeting locations, will be available at www.RRB.gov under either Informational Conference Program or Pre-Retirement Seminars.

Most railroad retirement annuities, like Social Security benefits, were scheduled to increase Jan. 1 on the basis of the rise in the Consumer Price Index (CPI) from the third quarter of 2016 to the corresponding period of 2017. The Railroad Retirement Board (RRB) reports that Tier I benefits, like Social Security benefits, will increase by 2 percent, which is the percentage of the CPI rise. Tier II benefits will go up by 0.7 percent. Vested dual benefit payments and supplemental annuities also paid by RRB are not adjusted for the CPI change. In January 2018, the average regular railroad retirement employee annuity will increase $42 a month to $2,711 and the average of combined benefits for an employee and spouse will increase $60 a month to $3,937. For those retirement-aged widow(er)s eligible for an increase, the average annuity will increase $24 a month to $1,353. However, widow(er)s whose annuities are being paid under the Railroad Retirement and Survivors’ Improvement Act of 2001 will not receive annual cost-of-living adjustments until their annuity amount is exceeded by the amount that would have been paid under prior law, counting all interim cost-of-living increases otherwise payable. Some 50 percent of the widow(er)s on the RRB’s rolls are being paid under the 2001 law. The cost-of-living increase is the largest since 2012, and follows a Tier I increase of 0.3 percent in January 2017. The RRB was mailing notices in December to all annuitants providing a breakdown of the annuity rates payable to them in January 2018.

Earning limit increases

The RRB also announced that railroad retirement annuitants subject to earnings restrictions can earn more in 2018 without having their benefits reduced as a result of increases in earnings limits indexed to average national wage increases. For those under full retirement age throughout 2018, the exempt earnings amount rises to $17,040 from $16,920 in 2017. For beneficiaries attaining full retirement age in 2018, the exempt earnings amount for the months before the month full retirement age is attained increases to $45,360 in 2018 from $44,880 in 2017. For those under full retirement age, the earnings deduction is $1 in benefits for every $2 of earnings over the exempt amount. For those attaining full retirement age in 2018, the deduction is $1 for every $3 of earnings over the exempt amount in the months before the month full retirement age is attained. For employee and spouse annuitants, full retirement age ranges from age 65 for those born before 1938 to age 67 for those born in 1960 or later. For survivor annuitants, full retirement age ranges from age 65 for those born before 1940 to age 67 for those born in 1962 or later. When applicable, earnings deductions are assessed on the Tier I and vested dual benefit portions of railroad retirement employee and spouse annuities, and the Tier I, Tier II, and vested dual benefit portions of survivor benefits. All earnings received for services rendered, plus any net earnings from self-employment, are considered when assessing deductions for earnings. Interest, dividends, certain rental income, or income from stocks, bonds, or other investments are not considered earnings. Retired employees and spouses, regardless of age, who work for their last pre-retirement non-railroad employer are also subject to an additional earnings deduction in their Tier II and supplemental benefits of $1 for every $2 in earnings up to a maximum reduction of 50 percent. This earnings restriction does not change from year to year and does not allow for an exempt amount. A spouse benefit is subject to reduction not only for the spouse’s earnings, but also for the earnings of the employee, regardless of whether the earnings are from service for the last pre-retirement non-railroad employer or other post-retirement employment. Special work restrictions continue to be applicable to disability annuitants in 2018. The monthly disability earnings limit increases to $920 in 2018 from $910 in 2017. Regardless of age and/or earnings, no railroad retirement annuity is payable for any month in which an annuitant (retired employee, spouse or survivor) works for a railroad employer or railroad union. More information about RRB benefits is available at the agency’s website at www.rrb.gov or by contacting the RRB toll free at 1-877-772-5772.

Certain portions of a railroad retirement annuity are treated differently for federal income tax purposes. The following questions and answers explain these differences and address the importance of individuals establishing accurate tax withholding from their annuities. Certain beneficiaries, including those retiring at age 60 with at least 30 years of service, and some occupational disability annuitants, need to pay close attention to changes in tax withholding when they turn age 62.

1.How are annuities paid under the Railroad Retirement Act treated under federal income tax laws? A railroad retirement annuity is a single payment comprised of one or more of the following components, depending on the annuitant’s age, the type of annuity being paid, and eligibility requirements: a Social Security Equivalent Benefit (SSEB) portion of tier I, a Non-Social Security Equivalent Benefit (NSSEB) portion of tier I, a tier II benefit, a vested dual benefit and a supplemental annuity. In most cases, part of a railroad retirement annuity is treated like a social security benefit for federal income tax purposes, while other parts of the annuity are treated like private pensions for tax purposes. Consequently, most annuitants are sent two tax statements from the Railroad Retirement Board (RRB) each January, even though they receive only a single annuity payment each month. 2.What information is shown on the railroad retirement tax statements sent to annuitants in January? One statement, Form RRB-1099 for U.S. citizens or residents (or Form RRB-1042S for nonresident aliens), shows the SSEB portion of tier I or special minimum guaranty payments made during the tax year, the amount of any such benefits that an annuitant may have repaid to the RRB during the tax year, and the net amount of these payments after subtracting the repaid amount. The amount of any offset for workers’ compensation and the amount of federal income tax withheld from these payments are also shown. The other statement, Form RRB-1099-R (for both U.S. citizens and nonresident aliens), shows the NSSEB portion of tier I, tier II, vested dual benefit and supplemental annuity paid to the annuitant during the tax year, and may show an employee contribution amount. The NSSEB portion of tier I along with tier II are considered contributory pension amounts and are shown as a single combined amount in the Contributory Amount Paid box (Item 4) on the statement. The vested dual benefit and supplemental annuity are considered noncontributory pension amounts and are shown as separate items on the statement. 3.Can annuitants request federal income tax withholding from their benefit payments? Yes, annuitants may request that federal income tax be withheld from their annuity payments. To add or change federal income taxes withheld from SSEB payments, an annuitant must complete Internal Revenue Service (IRS) Form W-4V, Voluntary Withholding Request, and send it to the RRB. To add or change the amount of federal taxes withheld from NSSEB payments, annuitants must file Form RRB W-4P, Withholding Certificate for Railroad Retirement Payments, and send it to the RRB. If an annuitant does not file a Form RRB W-4P with the RRB and the taxable annuity components exceed the IRS minimum mandatory withholding amount, taxes will automatically be withheld as if the annuitant were married and claiming three allowances. Railroad retirement benefits are not taxable by any state, so state tax withholding from railroad retirement payments is not possible. Annuitants that wish to add or change federal tax withholding from their annuity payments may contact the RRB for assistance. While the RRB may provide the necessary forms for withholding, it is the annuitant’s responsibility to determine how much federal income tax withholding is needed. Annuitants are encouraged to discuss the amount of withholding needed with a tax advisor or the IRS. 4.Which railroad retirement benefits are treated like social security benefits for federal income tax purposes? The SSEB portion of tier I (the part of a railroad retirement annuity equivalent to a social security benefit based on comparable earnings and included on Form RRB-1099) must be reported on an individual’s federal income tax return, and is treated for tax purposes the same way as a social security benefit. The amount of these benefits that may be subject to federal income tax, if any, depends on the beneficiary’s income. (To determine if any amount of the SSEB portion is taxable, please refer to IRS publication 915, Social Security and Equivalent Railroad Retirement Benefits.) If part of the SSEB is taxable, how much is taxable depends on the total amount of a beneficiary’s benefits and other income. Usually, the higher that total amount, the greater the taxable part of a beneficiary’s benefit. 5.Which railroad retirement benefits are treated like private pensions for federal income tax purposes? The NSSEB portion of tier I, tier II benefits, vested dual benefits and supplemental annuities are all treated like private pensions for federal income tax purposes. In some cases, primarily those in which early retirement benefits are payable to retired employees and spouses between ages 60 and 62, some occupational disability benefits, and other categories of unique RRB entitlements, the entire annuity may be treated like a private pension. This is because social security benefits based on age and service are not payable before age 62, social security disability benefit entitlement requires total disability, and the Social Security Administration does not pay some categories of beneficiaries paid by the RRB. 6. How are 60/30 annuity payments taxed? A railroad employee with 30 or more years of creditable rail service is eligible for a regular annuity based on age and service the first full month he or she is age 60. The employee’s spouse is also eligible for an annuity the first full month he or she is age 60. These “60/30” annuity payments are taxed as follows: 60/30 annuity payments before the employee or spouse is age 62:All benefits paid to an employee before age 62 are considered NSSEB and are fully taxable and reported on Form RRB-1099-R. This includes all tier I and tier II benefits and any supplemental annuity that might be payable. Spouse benefits are also fully taxable and reported on Form RRB-1099-R until both the employee and spouse are age 62. 60/30 annuity payments after the employee is age 62: Once the employee turns age 62, part of the tier I benefit is still considered NSSEB, but some is now considered SSEB because equivalent social security benefits are payable at age 62. Since these equivalent social security benefits paid at age 62 would be reduced for early retirement, while 60/30 benefits are not reduced, the RRB computes the portion of the tier I benefit comparable to that payable under social security, and reports the SSEB amount on Form RRB-1099. The SSEB portion of spouse benefits is calculated the same way, except the employee and spouse must both be at least 62 for spouse benefits to be considered SSEB. WARNING for 60/30 annuitants who begin receiving annuities before age 62:As noted previously, when the employee turns age 62 (or the spouse turns age 62, provided the employee is also at least age 62) the taxability of tier I benefits changes from all private pension-equivalent benefits to a split between SSEB and NSSEB portions. For many annuitants this means that the tax withholding in place will automatically decrease, and sometimes this change is significant. This is because any Form RRB W-4P on file with the RRB will not consider the SSEB portion of tier I in the withholding calculation. In many cases, the SSEB portion will be subject to taxation because of the total amount of the annuitant’s income, and the decrease in withholding may result in an insufficient amount of taxes being withheld. Notices are released to annuitants advising of the change in the withholding amount, and they are encouraged to discuss the issue with a tax advisor or the IRS to determine the correct amount of withholding for them. Annuitants often need to file a new tax withholding election form with the RRB to increase withholding following this change, otherwise they may face a larger tax liability than expected when filing federal income tax returns the following year. 7. Are occupational disability annuitants subject to the same change in tax withholding at age 62? Those occupational disability annuitants not qualified for a period of disability (also known as a “Disability Freeze”) as defined under the Social Security Act will similarly see the taxability of tier I benefits change at age 62. 8. Where can an annuitant find more information about the taxability of railroad retirement annuities? More information regarding the taxability of railroad retirement benefits can be found in RRB booklets TXB-25, Tax Withholding and Railroad Retirement Payments, and TXB-85, The Taxation of Railroad Retirement Act Annuities. These booklets are available on the agency’s website at www.rrb.gov or by contacting the RRB toll free at 1-877-772-5772. ### Information is also available on the IRS website at www.irs.gov. To learn more about how SSEB payments, repayments, and tax withholding amounts should be reported to the IRS, refer to IRS Publication 915, Social Security and Equivalent Railroad Retirement Benefits. For additional information about how pension payments, repayments and tax withholding should be reported to the IRS, or how NSSEB contributory amounts paid are taxed, refer to IRS Publication 575, Pension and Annuity Income, and/or IRS Publication 939, General Rule for Pensions and Annuities.

The U.S. Railroad Retirement Board (RRB) is reminding rail employees out of work due to Hurricane Harvey and its aftermath that they may qualify for unemployment benefits. To determine eligibility or file claims for benefits, affected railroaders should call the RRB’s toll-free telephone number (1-877-772-5772) or visit its website at www.rrb.gov. Rail workers who are out of work and without Internet or regular mail service may temporarily claim benefits by calling the RRB’s toll-free number until services are restored.

In order to file an application for benefits online via the website, an individual must have an Internet Services Account with the agency. For security purposes, first-time users must obtain a unique password, which they can do by clicking on the link for requesting a Password Request Code (PRC) in the Benefit Online Services login section of the www.rrb.gov home page.

Individuals who have already established an Internet Services Account and password can go online to file applications and claims for biweekly unemployment benefits, as well as conduct other business with the RRB over the Internet. For rail workers without power or Internet access, the RRB encourages them to call the agency toll-free at 1-877-772-5772.

Claimants can also find the address of the RRB office servicing their area and get information about their claims and benefit payments by calling this toll-free number. Most RRB offices are open to the public from 9:00 a.m. to 3:30 p.m. on Monday, Tuesday, Thursday, and Friday, and 9 a.m. to noon on Wednesday, except on Federal holidays. Field office locations can also be found online at www.rrb.gov.

Railroad unemployment benefits are normally paid for the number of days of unemployment over four in 14-day registration periods. The maximum daily benefit rate is currently $72. However, as a result of sequestration under the Budget Control Act of 2011, unemployment benefits are reduced by 6.9 percent through September 30, 2017, so the maximum benefit in a two-week period is $670.32. Also, during the first 14-day claim period in a benefit year, benefits are payable for each day of unemployment in excess of seven, rather than four, which basically creates a one-week waiting period.

To qualify for normal railroad unemployment benefits in the benefit year that began July 1, 2017, an employee must have had railroad earnings of at least $3,673.50 in calendar year 2016, counting no more than $1,455 for any month. Those who were first employed in the rail industry in 2016 must also have at least five months of creditable railroad service in that year.

Under certain conditions, employees with at least 10 years of service who do not qualify on the basis of their 2016 earnings may still be able to receive benefits. For example, employees who received normal benefits in the benefit year that ended June 30, 2017, might still be eligible for extended benefits. In addition, 10-year employees may be eligible for accelerated benefits if they had rail earnings of at least $3,637.50 in 2017, not counting earnings of more than $1,455 a month.

The Railroad Retirement Board (RRB) released its Informational Conference Schedule for September – December 2017. Check-in begins at 8:00 a.m. and programs begin promptly at 8:30 a.m. and end at 12:15 p.m. at all locations. Click here for a list of conferences. Online registration for each informational conference will be available 60 days prior to the date of the conference. Registration is available now for March and April conferences. Click here to register online.

The Railroad Retirement Board (RRB) administers the Railroad Unemployment Insurance Act, which provides two kinds of benefits for qualified railroaders: unemployment benefits for those who become unemployed but are ready, willing and able to work; and sickness benefits for those who are unable to work because of sickness or injury. Sickness benefits are also payable to female rail workers for periods of time when they are unable to work because of pregnancy and childbirth. A new benefit year begins each July 1.

The following questions and answers describe these benefits, their eligibility requirements, and how to claim them.

1.What are the eligibility requirements for railroad unemployment and sickness benefits in July 2017?

To qualify for normal railroad unemployment or sickness benefits, an employee must have had railroad earnings of at least $3,637.50 in calendar year 2016, counting no more than $1,455 for any month. Those who were first employed in the rail industry in 2016 must also have at least five months of creditable railroad service in 2016.

Under certain conditions, employees who do not qualify on the basis of their 2016 earnings may still be able to receive benefits in the new benefit year. Employees with at least 10 years of service (120 or more months of service) who received normal benefits in the benefit year ending June 30, 2017, may be eligible for extended benefits, and employees with at least 10 years of service (120 or more months of service) might qualify for accelerated benefits if they have rail earnings of at least $3,637.50 in 2017, not counting earnings of more than $1,455 a month.

In order to qualify for extended unemployment benefits, a claimant must not have voluntarily quit work without good cause and not have voluntarily retired. To qualify for extended sickness benefits, a claimant must not have voluntarily retired and must be under age 65.

To be eligible for accelerated benefits, a claimant must have 14 or more consecutive days of unemployment or sickness; not have voluntarily retired or, if claiming unemployment benefits, quit work without good cause; and, when claiming sickness benefits, be under age 65.

2.What is the daily benefit rate payable in the new benefit year beginning July 1, 2017?

Almost all employees will qualify for the maximum daily benefit rate of $72. Benefits are generally payable for the number of days of unemployment or sickness over four in 14-day claim periods, which yields $720 for each two full weeks of unemployment or sickness. Sickness benefits payable for the first 6 months after the month the employee last worked are subject to tier I railroad retirement payroll taxes, unless benefits are being paid for an on-the-job injury. (Claimants should be aware that as a result of a sequestration order under the Budget Control Act of 2011, the RRB will reduce unemployment and sickness benefits by 6.9 percent through September 30, 2017. As a result, the total maximum amount payable in a 2-week period covering 10 days of unemployment or sickness will be $670.32. The maximum amount payable for sickness benefits subject to tier I payroll taxes of 7.65 percent will be $619.04 over two weeks. Future reductions, should they occur, will be calculated based on applicable law.)

3.How long are these benefits payable?

Normal unemployment or sickness benefits are each payable for up to 130 days (26 weeks) in a benefit year. The total amount of each kind of benefit which may be paid in the new benefit year cannot exceed the employee’s railroad earnings in calendar year 2016, counting earnings up to $1,879 per month.

If normal benefits are exhausted, extended benefits are payable for up to 65 days (during 7 consecutive 14-day claim periods) to employees with at least 10 years of service (120 or more cumulative service months).

4.What is the waiting-period requirement for unemployment and sickness benefits?

Benefits are normally paid for the number of days of unemployment or sickness over four in 14-day registration periods. Initial sickness claims must also begin with four consecutive days of sickness. However, during the first 14-day claim period in a benefit year, benefits are only payable for each day of unemployment or sickness in excess of seven which, in effect, provides a one-week waiting period. (If an employee has at least five days of unemployment or five days of sickness in a 14-day period, he or she should still file for benefits.) Separate waiting periods are required for unemployment and sickness benefits. However, only one seven-day waiting period is generally required during any period of continuing unemployment or sickness, even if that period continues into a subsequent benefit year.

5.Are there special waiting-period requirements if unemployment is due to a strike?

If a worker is unemployed because of a strike conducted in accordance with the Railway Labor Act, benefits are not payable for days of unemployment during the first 14 days of the strike, but benefits are payable during subsequent 14-day periods.

If a strike is in violation of the Railway Labor Act, unemployment benefits are not payable to employees participating in the strike. However, employees not among those participating in such an illegal strike, but who are unemployed on account of the strike, may receive benefits after the first two weeks of the strike.

While a benefit year waiting period cannot count toward a strike waiting period, the 14-day strike waiting period may count as the benefit year waiting period if a worker subsequently becomes unemployed for reasons other than a strike later in the benefit year.

6.Can employees in train and engine service receive unemployment benefits for days when they are standing by or laying over between scheduled runs?

No, not if they are standing by or laying over between regularly assigned trips or they missed a turn in pool service.

7.Can extra-board employees receive unemployment benefits between jobs?

Yes, but only if the miles and/or hours they actually worked were less than the equivalent of normal full-time work in their class of service during the 14-day claim period. Entitlement to benefits would also depend on the employee’s earnings.

8.How would an employee’s earnings in a claim period affect his or her eligibility for unemployment benefits?

If a claimant’s earnings for days worked, and/or days of vacation, paid leave, or other leave in a 14-day registration period are more than a certain indexed amount, no benefits are payable for any days of unemployment in that period. That registration period, however, can be used to satisfy the waiting period.

Earnings include pay from railroad and nonrailroad work, as well as part-time work and self-employment. Earnings also include pay that an employee would have earned except for failure to mark up or report for duty on time, or because he or she missed a turn in pool service or was otherwise not ready or willing to work. For the benefit year that begins July 2017, the amount is $1,455, which corresponds to the base year monthly compensation amount used in determining eligibility for benefits in each year. Also, even if an earnings test applies on the first claim in a benefit year, this will not prevent the first claim from satisfying the waiting period in a benefit year.

On the other hand, earnings of no more than $15 a day from work which is substantially less than full-time and not inconsistent with the holding of normal full-time employment may be considered subsidiary remuneration and may not prevent payment of any days in a claim. However, a claimant must be sure to report all full and part-time work on each claim, regardless of the amount of earnings, so the RRB can determine whether the work affects benefits.

9.How does a person apply for and claim unemployment benefits?

Claimants can file their applications for unemployment benefits, as well as their subsequent biweekly claims, by mail or online.

To apply by mail, claimants must obtain an application from their labor organization, employer, local RRB office or the agency’s website at www.rrb.gov. The completed application should be mailed to the local RRB office as soon as possible and, in any case, must be filed within 30 days of the date on which the claimant became unemployed or the first day for which he or she wishes to claim benefits. Benefits may be lost if the application is filed late.

To file their applications — or their biweekly claims — online, claimants must first establish an RRB online account at www.rrb.gov. Instructions on how to do so are available by visiting the Benefit Online Services section of the RRB’s website. Employees are encouraged to establish online accounts while still employed so the account is ready if they ever need to apply for these benefits or use other select RRB Internet services. Employees who have already established online accounts do not need to do so again.

The local RRB field office reviews the completed application, whether it was submitted by mail or online, and notifies the claimant’s current railroad employer, and base-year employer, if different. The employer has the opportunity to provide information about the benefit application.

After the RRB office processes the application, biweekly claim forms are mailed to the claimant, and are also available on the RRB’s website, as long as he or she remains unemployed and eligible for benefits. Claim forms should be signed and sent on or after the last day of the claim. This can be done by mail or electronically. The completed claim must be received by an RRB office within 15 days of the end of the claim or the date the claim form was mailed to the claimant or made available online, whichever is later. Claimants must not file both a paper claim and an online claim form for the same period(s).

Only one application needs to be filed during a benefit year, even if a claimant becomes unemployed more than once. However, a claimant must, in such a case, request a claim form from an RRB office within 30 days of the first day for which he or she wants to resume claiming benefits. These claims may then be filed by mail or online.

10.How does a person apply for and claim sickness benefits?

An application for sickness benefits can be obtained from railroad labor organizations, railroad employers, any RRB office or the agency’s website. An application and a doctor’s statement of sickness are required at the beginning of each period of continuing sickness for which benefits are claimed. Claimants should make a special effort to have the doctor’s statement of sickness completed promptly since no claims can be paid without it.

The RRB suggests that employees keep an application on hand for use in claiming sickness benefits, and that family members know where the form is kept and how to use it. If an employee becomes unable to work because of sickness or injury, the employee should complete the application and then have his or her doctor complete the statement of sickness. Employees should note that they must indicate on the application whether they are applying for sickness benefits because they were injured at work or have a work-related illness. They must also indicate whether they have filed or expect to file a lawsuit or claim against a third party for personal injury. If a claimant receives sickness benefits for an injury or illness for which he or she is paid damages, it is important to be aware that the RRB is entitled to reimbursement of either the amount of the benefits paid for the injury or illness, or the net amount of the settlement, after deducting the claimant’s gross medical, hospital, and legal expenses, whichever is less.

If the employee is too sick to complete the application, someone else may do so. In such cases, a family member should also complete Form SI-10, “Statement of Authority to Act for Employee,” which accompanies the statement of sickness.

After completion, the forms should be mailed to the RRB’s headquarters in Chicago by the seventh day of the illness or injury for which benefits are claimed. However, applications received after 10 days but within 30 days of the first day for which an employee wishes to claim benefits are generally considered timely filed if there is a good reason for the delay. After the RRB receives the application and statement of sickness and determines eligibility, biweekly claim forms are mailed to the claimant for completion and return to an RRB field office for processing. The RRB also makes claim forms available for completion online by those employees who establish an online account. The claim forms must be received at the RRB within 30 days of the last day of the claim period, or within 30 days of the date the claim form was mailed to the claimant or made available online, whichever is later. Benefits may be lost if an application or claim is filed late.

Claimants are reminded that while claim forms for sickness benefits can be submitted online, applications must be returned to the RRB by mail. Doctors’ statements of sickness can be submitted by mail or fax. Faxes must include a cover sheet from the doctor’s office.

11.Is a claimant’s employer notified each time a biweekly claim for unemployment or sickness benefits is filed?

The Railroad Unemployment Insurance Act requires the RRB to notify the claimant’s base-year employer each time a claim for benefits is filed. That employer has the right to submit information relevant to the claim before the RRB makes an initial determination on the claim. In addition, if a claimant’s base-year employer is not his or her current employer, the claimant’s current employer is also notified. The RRB must also notify the claimant’s base-year employer each time benefits are paid to a claimant. The base-year employer may protest the decision to pay benefits. Such a protest does not prevent the timely payment of benefits. However, a claimant may be required to repay benefits if the employer’s protest is ultimately successful. The employer also has the right to appeal an unfavorable decision to the RRB’s Bureau of Hearings and Appeals.

The RRB also conducts checks with other Federal agencies and all 50 States, as well as the District of Columbia and Puerto Rico, to detect fraudulent benefit claims, and it checks with physicians to verify the accuracy of medical statements supporting sickness benefit claims.

12.How long does it take to receive payment?

Under the RRB’s Customer Service Plan, if a claimant filed an application for unemployment or sickness benefits, the RRB will release a claim form or a denial letter within 10 days of receiving his or her application. If a claim for subsequent biweekly unemployment or sickness benefits is filed, the RRB will certify a payment or release a denial letter within 10 days of the date the RRB receives the claim form. If the claimant is entitled to benefits, benefits will generally be paid within one week of that decision.

However, some claims for benefits may take longer to handle than others if they are more complex, or if an RRB office has to get information from other people or organizations. If this happens, claimants may expect an explanation and an estimate of the time required to make a decision.

Claimants who think an RRB office made the wrong decision about their benefits have the right to ask for review and to appeal. They will be notified of these rights each time an unfavorable decision is made on their claims.

13.How are payments made?

Railroad unemployment and sickness insurance benefits are paid by the U.S. Treasury’s Direct Deposit program. With Direct Deposit, benefit payments are made electronically to an employee’s bank, savings and loan, credit union or other financial institution. New applicants for unemployment and sickness benefits will be asked to provide information needed for Direct Deposit enrollment.

14.How can claimants get more information on railroad unemployment or sickness benefits?

Claimants with questions about unemployment or sickness benefits, or who are seeking information about their claims and benefit payments, can contact an RRB office by calling toll-free at 1-877-772-5772. Claimants can also access an online service, “View RUIA Account Statement” in the Benefit Online Services section of www.rrb.gov, which provides a summary of the unemployment and sickness benefits paid to them. To use this feature, claimants must first establish an online account.

Persons can find the address of the RRB office serving their area by calling 1-877-772-5772, or by visiting www.rrb.gov. Most RRB offices are open to the public on weekdays from 9:00 a.m. to 3:30 p.m., except on Wednesdays when offices are open from 9:00 a.m. to 12:00 p.m. RRB offices are closed on Federal holidays.

Each year, the U.S. Railroad Retirement Board (RRB) prepares a “Certificate of Service Months and Compensation” (Form BA-6) for every railroad employee with creditable railroad compensation in the previous calendar year. The RRB will mail the forms to employees during the first half of June. While every effort has been made to maintain current addresses for all active railroad employees, anyone with compensation reported in 2017 who has not received Form BA-6 by July 1, or needs a replacement, should contact an RRB field office by calling the agency toll-free at 1-877-772-5772.

Each year, the U.S. Railroad Retirement Board (RRB) prepares a “Certificate of Service Months and Compensation” (Form BA-6) for every railroad employee with creditable railroad compensation in the previous calendar year. The RRB will mail the forms to employees during the first half of June. While every effort has been made to maintain current addresses for all active railroad employees, anyone with compensation reported in 2017 who has not received Form BA-6 by July 1, or needs a replacement, should contact an RRB field office by calling the agency toll-free at 1-877-772-5772.