Designed for railroad employees and spouses planning to retire within five years, the pre-retirement seminars offered by the Railroad Retirement Board are designed to familiarize attendees with the retirement benefits available to them, and also guide them through the application process. Sponsored by the Office of the Labor Member, seminars are held at a number of locations annually. Registration is required to attend. Pre-Retirement Seminar Booklet RRB field service representatives conduct each pre-retirement seminar using a slide presentation covering the various benefits provided retired rail workers and their families. Attendees receive a program booklet of this presentation with detailed side notes and fact sheets. In addition to the program booklet, seminar attendees receive a retirement kit full of informational handouts and other helpful materials. Online and downloadable versions of items included with seminar kits are available on the RRB’s Educational Materials webpage.

Schedule and registration

Registration is required to ensure accommodations and materials for all attendees.

Unless otherwise noted, pre-retirement seminars begin at 8:30 a.m. and are held over the course of 4 hours. (Doors open for attendees 30 minutes before the seminar start time.)

Security screening is required for seminars hosted inside any Federal buildings. Bring a current, valid photo ID (issued by State/Federal Government); no weapons permitted.

Parking fee for seminars marked with *.

Attendees are encouraged to bring original records (or certified copies) of documents required in order to file a railroad retirement application (such as proof of age, marriage or military service), along with an additional copy of each item to leave with field service staff.

Please let the RRB know if you sign up for a seminar and become unable to attend.

Can’t join the RRB for a seminar, but still interested in learning about the railroad retirement program and application process? Please contact the RRB via Field Office Locatoror by calling toll-free (1-877-772-5772) for pre-retirement information or to schedule an appointment for individual retirement counseling at your local RRB field office.

The U.S. Railroad Retirement Board (RRB) has named Crystal Coleman as its director of programs. As a result, Ms. Coleman will be responsible for overseeing all operations to process and pay benefits administered by the agency. She will also be a member of the RRB’s executive committee, which is responsible for day-to-day operations of the agency and for making policy recommendations to the three-member board. At the time of her appointment, Ms. Coleman had served as the RRB’s deputy director of programs since November 2015. In that position, she served as the agency’s second in command on all program-related issues and operations to Dr. Michael A. Tyllas, who retired in December 2018 after more than 37 years of federal service. Prior to her appointment as deputy director of programs, Ms. Coleman was the deputy regional director of the employee benefits security administration (EBSA) in Dallas. As the number-two official in the regional office, she supervised senior staff and assisted in planning, developing, implementing and evaluating EBSA programs in the region. An agency within the U.S. Department of Labor, the EBSA assures the security of retirement, health and other workplace-related benefits of workers and their families. An EBSA employee for 24 years, Ms. Coleman previously served as both a supervisory and senior investigator in both Chicago and Los Angeles, as well as the Senior Advisor for Criminal Enforcement in Chicago, before assuming the deputy regional director position in October 2013. Before entering Federal service in 1991, she spent about 18 months as an economic development coordinator for the City of Chicago. A native and current resident of Chicago, Ms. Coleman attended Illinois State University in Normal, Ill., receiving a bachelor’s degree in communications (1982), and subsequently earned a master’s degree in business administration (1991) from Roosevelt University in Chicago. Her appointment was effective July 29.

The Railroad Retirement Board (RRB) administers the Railroad Unemployment Insurance Act, which provides two kinds of benefits for qualified railroaders: unemployment benefits for those who become unemployed but are ready, willing and able to work; and sickness benefits for those who are unable to work because of sickness or injury. Sickness benefits are also payable to female rail workers for periods of time when they are unable to work because of health conditions related to pregnancy, miscarriage or childbirth. A new benefit year begins each July 1.

The following questions and answers describe these benefits, their eligibility requirements and how to claim them.

1. What are the eligibility requirements for railroad unemployment and sickness benefits in July 2019?

To qualify for normal railroad unemployment or sickness benefits, an employee must have had railroad earnings of at least $3,900 in the calendar year 2018, counting no more than $1,560 for any month. Those who were first employed in the rail industry in 2018 must also have at least five months of creditable railroad service in 2018.

Under certain conditions, employees who do not qualify on the basis of their 2018 earnings may still be able to receive benefits in the new benefit year. Employees with at least 10 years of service (120 or more months of service) who received normal benefits in the benefit year ending June 30, 2019, may be eligible for extended benefits, and employees with at least 10 years of service (120 or more months of service) might qualify for accelerated benefits if they have rail earnings of at least $4,012.50 in 2019, not counting earnings of more than $1,605 a month.

In order to qualify for extended unemployment benefits, a claimant must not have voluntarily quit work without good cause and not have voluntarily retired. To qualify for extended sickness benefits, a claimant must not have voluntarily retired and must be under age 65.

To be eligible for accelerated benefits, a claimant must have 14 or more consecutive days of unemployment or sickness; not have voluntarily retired or, if claiming unemployment benefits, quit work without good cause; and, when claiming sickness benefits, be under age 65.

2. What is the daily benefit rate payable in the new benefit year beginning July 1, 2019?

Almost all employees will qualify for the maximum daily benefit rate of $78. Benefits are generally payable for the number of days of unemployment or sickness over four in 14-day claim periods, which yields $780 for each two full weeks of unemployment or sickness. Sickness benefits payable for the first 6 months after the month the employee last worked are subject to tier I railroad retirement payroll taxes, unless benefits are being paid for an on-the-job injury. (Claimants should be aware that as a result of a sequestration order under the Budget Control Act of 2011, the RRB will reduce unemployment and sickness benefits by 6.2 percent through September 30, 2019. As a result, the total maximum amount payable in a 2-week period covering 10 days of unemployment or sickness will be $731.64. The maximum amount payable for sickness benefits subject to tier I payroll taxes of 7.65 percent will be $675.67 over two weeks. Future reductions, should they occur, will be calculated based on applicable law.)

3. How long are these benefits payable?

Normal unemployment or sickness benefits are each payable for up to 130 days (26 weeks) in a benefit year. The total amount of each kind of benefit which may be paid in the new benefit year cannot exceed the employee’s railroad earnings in calendar year 2018, counting earnings up to $2,015 per month.

If normal benefits are exhausted, extended benefits are payable for up to 65 days (during seven consecutive 14-day claim periods) to employees with at least 10 years of service (120 or more cumulative service months).

4. What is the waiting-period requirement for unemployment and sickness benefits?

Benefits are normally paid for the number of days of unemployment or sickness over four in 14-day registration periods. Initial sickness claims must also begin with four consecutive days of sickness. However, during the first 14-day claim period in a benefit year, benefits are only payable for each day of unemployment or sickness in excess of seven which, in effect, provides a one-week waiting period. (If an employee has at least five days of unemployment or five days of sickness in a 14-day period, he or she should still file for benefits.) Separate waiting periods are required for unemployment and sickness benefits. However, only one seven-day waiting period is generally required during any period of continuing unemployment or sickness, even if that period continues into a subsequent benefit year.

5. Are there special waiting-period requirements if unemployment is due to a strike?

If a worker is unemployed because of a strike conducted in accordance with the Railway Labor Act, benefits are not payable for days of unemployment during the first 14 days of the strike, but benefits are payable during subsequent 14-day periods.

If a strike is in violation of the Railway Labor Act, unemployment benefits are not payable to employees participating in the strike. However, employees not among those participating in such an illegal strike, but who are unemployed on account of the strike, may receive benefits after the first two weeks of the strike.

While a benefit year waiting period cannot count toward a strike waiting period, the 14-day strike waiting period may count as the benefit year waiting period if a worker subsequently becomes unemployed for reasons other than a strike later in the benefit year.

6. Can employees in train and engine service receive unemployment benefits for days when they are standing by or laying over between scheduled runs?

No, not if they are standing by or laying over between regularly assigned trips or they missed a turn in pool service.

7. Can extra-board employees receive unemployment benefits between jobs?

Yes, but only if the miles and/or hours they actually worked were less than the equivalent of normal full-time work in their class of service during the 14-day claim period. Entitlement to benefits would also depend on the employee’s earnings.

8. How would an employee’s earnings in a claim period affect his or her eligibility for unemployment benefits?

If a claimant’s earnings for days worked, and/or days of vacation, paid leave or other leave in a 14-day registration period are more than a certain indexed amount, no benefits are payable for any days of unemployment in that period. That registration period, however, can be used to satisfy the waiting period.

Earnings include pay from railroad and nonrailroad work, as well as part-time work and self-employment. Earnings also include pay that an employee would have earned except for failure to mark up or report for duty on time, or because he or she missed a turn in pool service or was otherwise not ready or willing to work. For the benefit year that begins July 2019, the amount is $1,560, which corresponds to the base year monthly compensation amount used in determining eligibility for benefits in each year. Also, even if an earnings test applies on the first claim in a benefit year, this will not prevent the first claim from satisfying the waiting period in a benefit year.

On the other hand, earnings of no more than $15 a day from work which is substantially less than full-time and not inconsistent with the holding of normal full-time employment may be considered subsidiary remuneration and may not prevent payment of any days in a claim. However, a claimant must be sure to report all full and part-time work on each claim, regardless of the amount of earnings, so the RRB can determine if the work affects benefits.

9. How does a person apply for and claim unemployment benefits?

Employees can apply for and claim unemployment benefits online or by mail.

Individuals who have established an account at RRB.gov can log in to conveniently file their applications and their biweekly claims online. Employees are encouraged to establish their accounts while still working to expedite the filing process for future unemployment benefits, and for access to other online services.

To apply by mail, claimants must obtain an Application for Unemployment Benefits (Form UI-1) from RRB.gov, any RRB field office, their labor organization or employer. The completed application should be mailed to the local RRB office as soon as possible and, in any case, must be filed within 30 days from the date the claimant became unemployed or the first day for which he or she wishes to claim benefits. Benefits may be lost if the application is filed late. Claimants who know in advance that they will be filing an unemployment application or claim late should include a signed statement explaining why they are unable to meet the required time frame.

The local RRB field office reviews the completed application, whether it was submitted online or by mail, and notifies the claimant’s current railroad employer, and base-year employer, if different. The employer has the right to provide information about the benefit application.

After processing the application, biweekly claim forms are made available on the RRB’s website and are mailed to the claimant, as long as he or she remains unemployed and eligible for benefits. Claim forms should be signed and sent on or after the last day of the claim. This can be done online or by mail. The completed claim must be received by the RRB within 15 days of the end of the claim period, or within 15 days of the date the claim form was made available online or mailed to the claimant, whichever is later. Claimants must not file both an online and a paper claim form for the same period(s). Once an individual submits a claim online, all subsequent claim forms will be made available online only, and will no longer be mailed.

Only one application needs to be filed during a benefit year, even if a claimant becomes unemployed more than once. However, a claimant must, in such a case, request a claim form from the RRB within 30 days of the first day for which he or she wants to resume claiming benefits. These claims may then be filed online or by mail.

10. How does a person apply for and claim sickness benefits?

An Application for Sickness Benefits (SI-1a) can be obtained from RRB.gov, any RRB field office, railroad labor organizations or railroad employers. An application including a doctor’s statement of sickness is required at the beginning of each period of continuing sickness for which benefits are claimed. Claimants should make a special effort to have the doctor’s statement of sickness completed promptly since claims cannot be paid without it.

The RRB suggests that employees keep an application for sickness benefits on hand, and that family members know where the form is kept and how to use it. If an employee becomes unable to work because of sickness or injury, the employee should complete the application and then have his or her doctor complete the Statement of Sickness (SI-1b). If a claimant receives sickness benefits for an injury or illness for which he or she is paid damages, it is important to be aware that the RRB is entitled to reimbursement of either the amount of the benefits paid for the injury or illness, or the net amount of the settlement, after deducting the claimant’s gross medical, hospital and legal expenses, whichever is less.

If the employee is too sick to complete the application, someone else may do so. In such cases, a family member should also complete a Statement of Authority to Act for Employee (Form SI-10), which accompanies the statement of sickness.

After completion, the forms should be mailed to the RRB’s headquarters in Chicago within 10 days from when the employee became sick or injured. However, applications received after 10 days but within 30 days of the first day for which an employee wishes to claim benefits are generally considered timely filed if there is a good reason for the delay. Upon receipt, the RRB will process the application and determine if the employee is eligible for sickness benefits.

After processing the application, the RRB provides biweekly claims to the qualified employee as long as he or she is eligible for benefits and remains unable to work due to illness or injury. Biweekly claims are made available for completion online (by those with anaccount at RRB.gov) and mailed to the claimant. Completed claim forms must be received at the RRB within 30 days of the last day of the claim period, or within 30 days of the date the claim form was made available online or mailed to the claimant, whichever is later. Benefits may be lost if an application or claim is filed late. Claimants who know in advance that they will be filing a sickness application or claim late should include a signed statement explaining why they are unable to meet the required time frame.

As with claims for unemployment benefits, once a claim for sickness benefits is submitted online, all subsequent claims will be made available online only, and will no longer be mailed.

Claimants are reminded that while claim forms for sickness benefits can be submitted online, applicationsmust bemailed to the RRB. Statements of sickness may be mailed with the sickness application or faxed directly from the doctor’s office to the RRB at 312-751-7185. Faxes must include a cover sheet from the doctor’s office.

11. Is a claimant’s employer notified each time a biweekly claim for unemployment or sickness benefits is filed?

The Railroad Unemployment Insurance Act requires the RRB to notify the claimant’s base-year employer each time a claim for benefits is filed. That employer has the right to submit information relevant to the claim before the RRB makes an initial determination on the claim. In addition, if a claimant’s base-year employer is not his or her current employer, the claimant’s current employer is also notified. The RRB must also notify the claimant’s base-year employer each time benefits are paid to a claimant. The base-year employer may protest the decision to pay benefits. Such a protest does not prevent the timely payment of benefits. However, a claimant may be required to repay benefits if the employer’s protest is ultimately successful. The employer also has the right to appeal an unfavorable decision to the RRB’s Bureau of Hearings and Appeals.

The RRB also conducts checks with other Federal agencies and all 50 states, as well as the District of Columbia and Puerto Rico, to detect fraudulent benefit claims, and it checks with physicians to verify the accuracy of medical statements supporting sickness benefit claims.

12. How long does it take to receive payment?

Under the RRB’s Customer Service Plan, if a claimant files an application for unemployment or sickness benefits, the RRB will release a claim form or a denial letter within 10 days of receiving his or her application. If a claim for subsequent biweekly unemployment or sickness benefits is filed, the RRB will certify a payment or release a denial letter within 10 days of the date the RRB receives the claim form. If the claimant is entitled to benefits, his or her benefits will generally be paid within one week of that decision.

However, some claims for benefits may take longer to handle than others if they are more complex, or if an RRB office has to get information from other people or organizations. If a claimant does not receive a decision notice or payment within the specified time period, he or she may expect an explanation for the delay and an estimate of the time required to make a decision.

Claimants who think an RRB office made the wrong decision about their benefits have the right to ask for a review and to appeal. They will be notified of these rights each time an unfavorable decision is made on their claims.

13. How are payments made?

Railroad unemployment and sickness insurance benefits are paid by direct deposit. With direct deposit, benefit payments are made electronically to an employee’s bank, savings and loan, credit union or other financial institution. New applicants for unemployment and sickness benefits will be asked to provide information needed for direct deposit enrollment.

14. How can claimants get more information on their railroad unemployment or sickness claims?

Claimants with online accounts at RRB.gov can log in to view their individual railroad unemployment insurance account statement. This statement displays the type and amount of the claimant’s last five benefit payments, the claim period for which the payments were made, and the dates that the payments were approved. Individuals can also confirm the RRB’s receipt of applications and claims.

In addition, claimants can call the agency toll-free at 1-877-772-5772 to access the RRB’s automated HelpLine service which provides information about the status of unemployment and sickness claims or payments 24 hours a day, 7 days a week. Individuals with questions about unemployment or sickness benefits, or who need information about their specific claims and benefit payments, can also contact an RRB office by calling the toll-free number.

Persons can find the address of the RRB office serving their area by visiting RRB.gov and clicking on Field Office Locator, or by calling the RRB’s HelpLine service and selecting the appropriate option from the automated menu. Most RRB offices are open to the public on weekdays from 9:00 a.m. to 3:30 p.m., except on Wednesdays when offices are open from 9:00 a.m. to 12:00 p.m. All RRB offices are closed on Federal holidays.

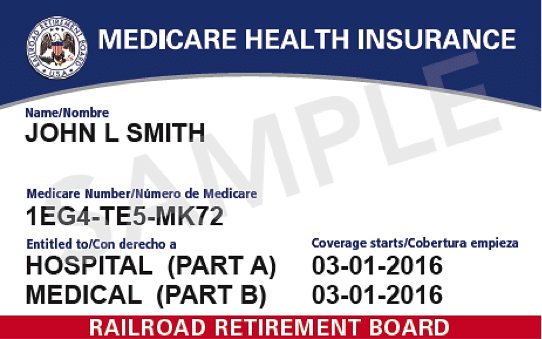

Last July, the Railroad Retirement Board (RRB) mailed approximately 450,000 new Railroad Medicare cards with new Medicare Numbers. The new Medicare Numbers, which are unique to each person with Railroad Medicare and do not contain Social Security Number (SSNs), replace the former Health Insurance Claim Numbers (HICNs). Providers can bill claims to Medicare with either a HICN or a new Medicare Number through December 31, 2019. At this time, approximately 70% of the Railroad Medicare claims received are submitted with Medicare Numbers. Beginning January 1, 2020, all providers will be required to file claims with Medicare Numbers only. When it’s time for a doctor’s appointment or other Medicare service, be sure to take your new card with you. Your provider’s office knows everyone should have a new Medicare Number, and they will need to keep a record of your Medicare Number so they can bill Railroad Medicare correctly. If your provider does not have a copy of your card, they may be able to look up your information with their local Medicare Administrative Contractor (MAC) or with Palmetto GBA Railroad Medicare through our online provider portals. These portals give authorized providers access to claims history, eligibility and more. The portals also contain a tool that allows providers to look up a Medicare Number with the following patient information:

Last Name

First Name

Date of Birth

Social Security Number

Please note that in order to use the tool to look up your Medicare Number, a provider must have your Social Security Number. If you do not want to give a provider your SSN, allow them to have a copy of your card or verbally give them your Medicare Number. If you have not used your card yet, you are making it much more difficult for your providers to file claims timely. One of the reasons for having the new cards was to give protection from identity theft. One way to do that is to be very selective when giving your personal information to a trusted entity (your doctor, insurers, etc.). When verbally giving your Medicare Number to a provider, or to a Customer Service Advocate when you call Railroad Medicare, make sure to read it correctly. Medicare Numbers have 11 characters and contain numbers and uppercase letters only. They do not contain the letters S, L, O, I, B or Z. Characters one, four, seven, 10 and 11 will always be a number. The second, fifth, eighth and ninth characters will always be a letter. The third and sixth characters will be a letter or a number. Sample RRB Medicare Card: If you are enrolled in a Medicare Advantage Plan, your new Medicare card does not replace your plan’s identification card. You will continue to use your plan’s ID card to receive your Medicare benefits. If you did not receive your new Medicare Card with your new Medicare Number, you can call Palmetto’s Beneficiary Contact Center at 800-833-4455 or the Railroad Retirement Board at 877-772-5772. Have questions? If you have questions about new Medicare cards or Medicare Numbers, please call Palmetto GBA’s Beneficiary Contact Center at 800-833-4455, Monday through Friday, from 8:30 a.m. to 7 p.m. ET. You are encouraged to sign up for email updates. To do so, click ‘Listservs’ on the top banner on the Palmetto website at www.PalmettoGBA.com/RR/Me. You are also encouraged to use the beneficiary portal, MyRRMed, which is located at www.PalmettoGBA.com/MyRRMed.

Rights to benefits under the Railroad Retirement Act also carry responsibilities for reporting events that may affect the payment of these benefits to the employee or to members of the employee’s family. If these events are not reported, benefit overpayments can occur that have to be repaid, sometimes with interest and penalties. Events that can affect the payment of a Railroad Retirement annuity and result in overpayments if not promptly reported include:

entitlement to Social Security or certain other benefits, and changes in the amount of such benefit payments;

post-retirement work activity and the receipt of earnings by age and service annuitants;

post-retirement work activity, whether earnings are received or not, by disability annuitants;

the death of an annuitant;

a change in marital status;

a child leaving the care of a spouse or widow(er);

a student ceasing full-time school attendance.

The following questions and answers describe how these events affect Railroad Retirement benefits and what should be done to prevent overpayments.

How can the awarding of Social Security benefits result in a Railroad Retirement annuity overpayment?

The Tier I portion of a Railroad Retirement annuity is based on both the Railroad Retirement and Social Security credits acquired by an employee and figured under Social Security formulas. It approximates what Social Security would pay if railroad work were covered by Social Security. Tier I benefits are, therefore, reduced by the amount of any actual Social Security benefit paid on the basis of non-railroad employment, in order to prevent a duplication of benefits based on the same earnings. The Tier I dual benefit reduction also applies to the annuity of an employee qualified for Social Security benefits on the earnings record of another person, such as a spouse. And, the Tier I portion of a spouse, divorced spouse or survivor annuity is reduced for any Social Security entitlement, even if the Social Security benefit is based on the spouse’s, divorced spouse’s or survivor’s own earnings. These reductions follow principles of Social Security law which limit payment to the higher of any two or more benefits payable to an individual at one time. If a Railroad Retirement annuitant is also awarded a Social Security benefit, in most cases a combined monthly dual benefit payment will be issued by the Railroad Retirement Board (RRB). The Social Security Administration determines the amount of the Social Security benefit due, and the RRB determines the amount of the Railroad Retirement annuity due. (As stated above, the Tier I portion of a Railroad Eetirement annuity is reduced by the amount of the Social Security benefit due.) A person should notify the RRB when he or she files for Social Security benefits. If the Social Security Administration begins paying benefits directly to a Railroad Retirement annuitant without the RRB’s knowledge, a Tier I overpayment will occur. This frequently happens when a railroad employee’s spouse or widow(er) is awarded Social Security benefits not based on the employee’s earnings. Also, annuitants who are receiving their Social Security benefits directly from the Social Security Administration must notify the RRB if their Social Security benefits are subsequently increased for any reason other than annual cost-of-living increases, such as a recomputation to reflect post-retirement earnings. As such recomputations are usually retroactive, they can result in substantial Tier I overpayments. While Social Security benefit information is provided to the RRB as a result of routine information exchanges between the RRB and the Social Security Administration, it will generally not be provided in time to avoid such a benefit overpayment.

What other types of benefit payments, besides Social Security benefits, require dual benefit reductions in a Railroad Retirement annuity?

For employees first eligible for a Railroad Retirement annuity and a federal, state or local government pension after 1985, there may be a reduction in Tier I for receipt of a public pension based, in part or in whole, on employment not covered by Social Security or Railroad Retirement after 1956. This may also apply to certain other payments not covered by Social Security, such as payments from a non-profit organization or from a foreign government or a foreign employer. However, it does not include military service pensions, payments by the Department of Veterans Affairs or certain benefits payable by a foreign government as a result of a totalization agreement between that government and the United States. The Tier I portion of a spouse or widow(er)’s annuity may also be reduced for receipt of any federal, state or local government pension separately payable to the spouse or widow(er) based on her or his own earnings. The reduction generally does not apply if the employment on which the public pension is based was covered under the Social Security Act throughout the last 60 months of public employment. In addition, most military service pensions and payments from the Department of Veterans Affairs will not cause a reduction. Pensions paid by a foreign government or interstate instrumentality will also not cause a reduction. If an employee is receiving a disability annuity, Tier I benefits for the employee and spouse may, under certain circumstances, be reduced for receipt of workers’ compensation or public disability benefits. If annuitants become entitled to any of the above payments, they should promptly notify the RRB. If there is any question as to whether a payment requires a reduction in an annuity, an RRB field office should be contacted.

Can post-retirement work activity and earnings cause Railroad Retirement overpayments?

Unreported post-retirement work activity and earnings in non-railroad employment (including self-employment) are a major cause of overpayments in Railroad Retirement annuities. Like Social Security benefits, Railroad Retirement Tier I benefits paid to employees and spouses, plus Tier I and Tier II benefits paid to survivors, are subject to deductions if post-retirement earnings exceed certain exempt amounts, which increase annually. (For information on how post-retirement work activity and earnings affect disability annuitants, please see Question 4.) These earnings deductions do not apply to those who have attained full Social Security retirement age. Under the Social Security Act, full retirement age for employees and spouses is age 66 for those born from 1943 through 1954 and gradually increases to age 67 for those born in 1960 or later. Full retirement age for survivor annuitants ranges from age 66 for those born from 1945 through 1956 to age 67 for those born in 1962 or later. For those under full retirement age throughout 2019, the exempt earnings amount is $17,640. For beneficiaries attaining full retirement age in 2019, the exempt earnings amount is $46,920 for the months before the month full retirement age is attained. Prior to the calendar year in which full retirement age is attained, the earnings deduction is $1 in benefits for every $2 of earnings over the exempt amount. For those attaining full retirement age during a calendar year, the deduction is $1 for every $3 of earnings over the exempt amount in the months before the month full retirement age is attained. Annuitants who work after retirement and expect that their earnings for a year will be more than the annual exempt amount must promptly notify the nearest RRB field office and furnish an estimate of their expected earnings. This way their annuities can be adjusted to take the excess earnings into consideration and prevent an overpayment. Annuitants whose original estimate changes significantly during the year, either upwards or downwards, should also notify the RRB. Retired employees and spouses, regardless of age, who work for their last pre-retirement non-railroad employer are also subject to an earnings deduction in their Tier II and Railroad Retirement supplemental annuity benefits, if applicable, of $1 for every $2 in earnings up to a maximum reduction of the lesser of 50 percent of the earnings or Tier II and supplemental benefits combined. This earnings restriction does not change from year to year and does not allow for an exempt amount. Retired employees and spouses should therefore promptly notify the RRB if they return to employment for their last pre-retirement non-railroad employer or if the amount of their earnings from such employment changes. A spouse benefit is subject to reductions not only for the spouse’s earnings, but also for the earnings of the employee, regardless of whether the earnings are from service for the last pre-retirement non-railroad employer or any other post-retirement employment. An annuity paid to a divorced spouse may continue despite the employee’s work activity. However, the employee’s non-railroad earnings over the annual earnings exempt amount may reduce a divorced spouse benefit.

How do post-retirement work activity and earnings affect disability annuities?

Any work performed by a disabled annuitant — whether for payment or not — may be considered an indication of recovery from disability and therefore must be reported promptly to avoid potential overpayments. In addition, special restrictions limiting earnings to $950 per month in 2019, exclusive of disability-related work expenses, apply to disabled Railroad Retirement employee annuitants. These disability work restrictions apply until the disabled employee annuitant attains full retirement age which, as stated earlier, ranges from age 66 to age 67, depending on the year of birth. These work restrictions apply even if the annuitant has 30 years of railroad service. Also, a disabled employee annuitant who works for his or her last pre-retirement non-railroad employer would be subject to the additional earnings deduction that applies in these cases.

What effect does railroad work have on an annuity?

No Railroad Retirement annuity is payable for any month in which an employee, spouse or survivor annuitant performs compensated service for a railroad or railroad union. This includes local lodge compensation for more than $24.99 in a calendar month, and work by a local lodge or division secretary collecting insurance premiums, regardless of the amount of salary.

What should be done when a Railroad Retirement annuitant dies?

The RRB should be notified immediately upon the death of any retirement or survivor annuitant. Payment of a Railroad Retirement annuity stops upon an annuitant’s death and the annuity is not payable for any day in the month of death. This is true regardless of how late in the month death occurs and there is no provision for prorating such a payment. Any payments received after the annuitant’s death must be returned. The sooner the RRB is notified, the less chance there is of payments continuing and an overpayment accruing. The RRB would also determine whether any survivor benefits due are payable by the RRB or the Social Security Administration.

What are some other events that can affect payments to auxiliary beneficiaries, such as spouses, divorced spouses and widow(er)s?

A spouse or divorced spouse must immediately notify the RRB if the railroad employee upon whose service the annuity is based dies. A spouse must notify the RRB if her or his marriage to the railroad employee ends in divorce or annulment and a widow(er) or divorced spouse must notify the RRB if she or he remarries. Also, benefits paid to spouses, widow(er)s and surviving divorced spouses that are based on the beneficiary caring for the employee’s unmarried child are normally terminated by the RRB when the child attains age 18 (age 16 for a surviving divorced spouse) or if a disabled child over age 18 (age 16 for a surviving divorced spouse) recovers from the disability. Therefore, the RRB must be notified if the child leaves the beneficiary’s care or marries. Benefits are also payable to an unmarried child age 18 in full-time attendance at an elementary or secondary school or in approved home schooling until the student attains age 19 or the end of the school term in progress when the student attains age 19. (In most cases where a student attains age 19 during the school term, benefits are limited to the two months following the month age 19 is attained.) These benefits will be terminated earlier if the student marries, graduates or ceases full-time attendance. Therefore, the RRB must be notified promptly to prevent an overpayment.

Can an annuitant contest a decision that he or she has been overpaid?

Annuitants who believe a decision regarding a benefit overpayment is incorrect may ask for reconsideration and/or waiver of the overpayment. If not satisfied with the result of the initial review, the annuitant may appeal to the RRB’s Bureau of Hearings and Appeals. Further appeals can be carried to the three-member board itself and beyond the board to federal courts. Annuitants are told about these appeal rights any time a decision is made regarding a benefit overpayment.

How can an annuitant find out if an event might affect his or her Railroad Retirement benefit payments?

Individuals should contact an RRB field office to determine if an event will affect their benefit payments. In any situation, the best rule is “If in doubt, report.” A Field Office Locator at RRB.gov provides easy access to every field office webpage where the street address and other service information is posted, as well as the option to email an office directly using the feature labeled Send a Secure Message. The agency’s toll-free number, 1-877-772-5772, is equipped with an automated menu offering a variety of service options, including being transferred to an office to speak with a representative, leave a message or find the address of a local field office. The agency also maintains a TTY number, 312-751-4701, to accommodate those with hearing or speech impairments. Most RRB offices are open to the public on weekdays from 9 a.m. to 3:30 p.m., except on Wednesdays when offices are open from 9 a.m. to noon. RRB offices are closed on federal holidays.

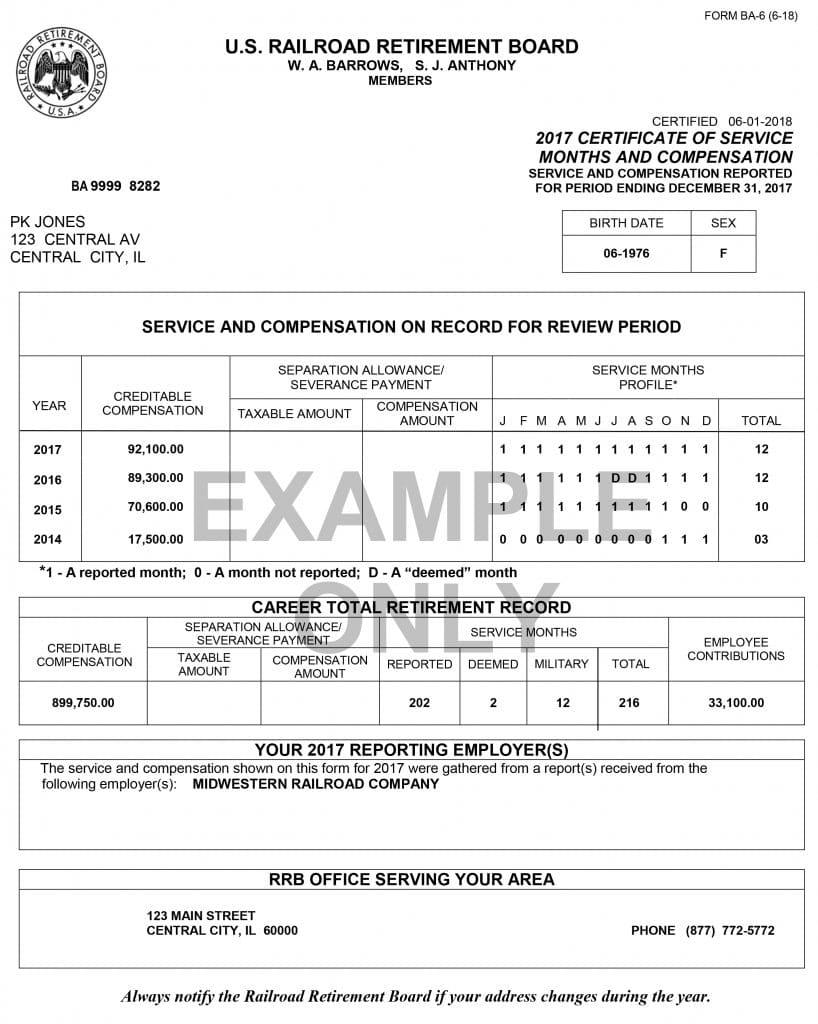

Each year, the U.S. Railroad Retirement Board (RRB) prepares a “Certificate of Service Months and Compensation” (Form BA-6) for every railroad employee with creditable railroad compensation in the previous calendar year. The RRB will mail the forms to employees during the first half of June. While every effort has been made to maintain current addresses for all active railroad employees, anyone with compensation reported in 2018 who has not received Form BA-6 by July 1, or needs a replacement, should contact an RRB field office by calling the agency toll-free at 1-877-772-5772. Form BA-6 provides employees with a record of their Railroad Retirement service and compensation, and the information shown is used to determine whether an employee qualifies for benefits and the amount of those benefits. It is important that employees review their Form BA-6 to see whether their own records of service months and creditable compensation agree with the figures shown on the form. In checking the 2018 compensation total, employees should be aware that only annual earnings up to $128,400 were creditable for Railroad Retirement purposes in that year, and that $128,400 is the maximum amount shown on the form. To assist employees in reviewing their service credits, the form also shows service credited on a month-by-month basis for 2017, 2016, and 2015, when the creditable compensation maximum was $127,200 for 2017 and $118,500 for both 2016 and 2015. The form also identifies the employer(s) reporting the employee’s 2018 service and compensation. Besides the months of service reported by employers, Form BA-6 shows the number of any additional service months deemed by the RRB. Deemed service months may be credited under certain conditions for an employee who did not work in all 12 months of the year, but had creditable Tier II earnings exceeding monthly prorations of the creditable Tier II earnings maximum for the year. However, the total of reported and deemed service months may never exceed 12 in a calendar year, and no service months, reported or deemed, can be credited after retirement, severance, resignation, discharge or death. The form also indicates the number of months of verified military service creditable as service under the Railroad Retirement Act, if the service was previously reported to the RRB. Employees are encouraged to submit proofs of age and/or military service in advance of their actual retirement. Filing these proofs with the RRB in advance will streamline the benefit application process and prevent payment delays. For employees who received separation or severance payments, the section of the form designated “Taxable Amount” shows the amounts reported by employers of any separation allowance or severance payments that were subject to Railroad Retirement Tier II taxes. This information is shown on the form because a lump sum, approximating part or all of the Tier II taxes deducted from such payments made after 1984 which did not provide additional Tier II credits, may be payable by the RRB upon retirement to qualified employees or to survivors if the employee dies before retirement. The amount of an allowance included in an employee’s regular compensation is shown under “Compensation Amount.” Form BA-6 also shows, in the section designated “Employee Contributions,” the cumulative amount of Tier II Railroad Retirement payroll taxes paid by the employee over and above Tier I Social Security equivalent payroll taxes. While the RRB does not collect or maintain payroll tax information, the agency computes this amount from its compensation records in order to advise retired employees of their payroll tax contributions for federal income tax purposes. Employees should check their name, address, birth date and sex shown at the top of the form. If the form shows the birth date as 99-9999 and the gender code is “U” (for unknown), it means the RRB is verifying his or her Social Security number with the Social Security Administration. Otherwise, if the personal identifying information is incorrect or incomplete (generally a case where the employee’s surname has more than 10 letters and the form shows only the first 10 letters) or the address is not correct, the employee should contact an RRB field office. The field office can then correct the RRB’s records. Any other discrepancies in Form BA-6 should be reported promptly in writing to:

Protest Unit-CESC U.S. Railroad Retirement Board 844 North Rush Street Chicago, Illinois 60611-1275

The employee must include his or her Social Security number in the letter. Form BA-6 also explains what other documentation and information should be provided. The law limits to four years the period during which corrections to service and compensation amounts can be made. For most employees, the address of the RRB office serving their area is provided on the form along with the RRB’s nationwide toll-free number (1-877-772-5772). RRB field offices are open to the public on weekdays from 9:00 a.m. to 3:30 p.m., except on Wednesdays when offices are open from 9:00 a.m. to 12:00 p.m. RRB offices are closed on Federal holidays.

The federal Medicare program provides hospital and medical insurance protection for Railroad Retirement annuitants and their families, just as it does for Social Security beneficiaries. Medicare has the following parts:

Medicare Part A (hospital insurance) helps pay for inpatient care in hospitals and skilled nursing facilities (following a hospital stay), some home health care services and hospice care. Part A is financed through payroll taxes paid by employees and employers.

Medicare Part B (medical insurance) helps pay for medically-necessary services like doctors’ services and outpatient care. Part B also helps cover some preventive services. Part B is financed by premiums paid by participants and by federal general revenue funds.

Medicare Part C (Medicare Advantage Plans) is another way to get Medicare benefits. It combines Part A, Part B, and sometimes, Part D (prescription drug) coverage. Medicare Advantage Plans are managed by private insurance companies approved by Medicare.

Medicare Part D (Medicare prescription drug coverage) offers voluntary insurance coverage for prescription drugs through Medicare prescription drug plans and other health plan options.

The following questions and answers provide basic information on Medicare eligibility and coverage, as well as other information on the Medicare program. 1. Who is eligible for Medicare? All Railroad Retirement beneficiaries age 65 or over and other persons who are directly or potentially eligible for Railroad Retirement benefits are covered by the program. Although the age requirements for some unreduced Railroad Retirement benefits have risen just like the Social Security requirements, beneficiaries are still eligible for Medicare at age 65. Coverage before age 65 is available for disabled employee annuitants who have been entitled to monthly benefits based on total disability for at least 24 months and have a disability insured status under Social Security law. There is no 24-month waiting period for those who have ALS (Amyotrophic Lateral Sclerosis), also known as Lou Gehrig’s disease. If entitled to monthly benefits based on an occupational disability, and the individual has been granted a disability freeze, he or she is eligible for Medicare starting with the 30th month after the freeze date or, if later, the 25th month after he or she became entitled to monthly benefits. If receiving benefits due to occupational disability and the person has not been granted a disability freeze, he or she is generally eligible for Medicare at age 65. (The standards for a disability freeze determination follow Social Security law and are comparable to the medical criteria a person must meet to be granted a total disability.) Under certain conditions, spouses, divorced spouses, surviving divorced spouses, widow(er)s, or a dependent parent may be eligible for Medicare hospital insurance based on an employee’s work record when the spouse, etc., turns 65. Also, disabled widow(er)s under 65, disabled surviving divorced spouses under 65, and disabled children may be eligible for Medicare, usually after a 24-month waiting period. Medicare coverage at any age on the basis of permanent kidney failure requiring hemodialysis or receipt of a kidney transplant is also available to employee annuitants, employees who have not retired but meet certain minimum service requirements, spouses and dependent children. The Social Security Administration has jurisdiction over Medicare in these cases. Therefore, a Social Security office should be contacted for information on coverage for kidney disease. 2. How do persons enroll in Medicare? If a retired employee or a family member is receiving a Railroad Retirement annuity, enrollment for both Medicare Part A and Part B is generally automatic and coverage begins when the person reaches age 65. For beneficiaries who are totally disabled, both Medicare Part A and Part B start automatically with the 30th month after the beneficiary became disabled or, if later, the 25th month after the beneficiary became entitled to monthly benefits. Even though enrollment is automatic, an individual may decline Part B; this does not prevent him or her from applying for Part B at a later date. However, premiums may be higher if enrollment is delayed. (See question five for more information on delayed enrollment.) If an individual is eligible for, but not receiving an annuity, he or she should contact the nearest Railroad Retirement Board (RRB) office before attaining age 65 and apply for both Part A and Part B. (This does not mean that the individual must retire, if working.) The best time to apply is during the three months before the month in which the individual reaches age 65. He or she will then have both Part A and Part B protection beginning with the month age 65 is reached. If the individual does not enroll for Part B in the three months before attaining age 65, he or she can enroll in the month age 65 is reached, or during the three months that follow, but there will be a delay of 1 to 3 months before Part B is effective. Individuals who do not enroll during this “initial enrollment period” may sign up in any “general enrollment period” (January 1 – March 31 each year). Coverage for such individuals begins July 1 of the year of enrollment. 3. Are there costs associated with Medicare Part A (hospital insurance)? Yes. While individuals don’t have to pay a premium to receive Medicare Part A, recipients of Part A benefits are billed by the hospital for a deductible amount ($1,364 in 2019), as well as any coinsurance amount due and any noncovered services. The remainder of the bill from the hospital, as well as bills for services in skilled nursing facilities or home health visits, is sent to Medicare to pay its share. 4. What are the costs associated with Medicare Part B (medical insurance)? Anyone eligible for Medicare hospital insurance (Part A) can enroll in Medicare medical insurance (Part B) by paying a monthly premium. The standard premium is $135.50 in 2019. However, some Medicare beneficiaries will not pay this amount because of a provision in the law that states Part B premiums for current enrollees cannot increase by more than the amount of the cost-of-living increase for Social Security (Railroad Retirement Tier I) benefits. Since that adjustment was 2.8 percent for 2019, about 2 million Medicare beneficiaries saw an increase in their Part B premiums, but still pay less than $135.50. The standard premium amount applies to new enrollees in the program, and certain beneficiaries who pay higher premiums based on their modified adjusted gross income. Monthly premiums for some beneficiaries are greater, depending on a beneficiary’s or married couple’s modified adjusted gross income. The income-related Part B premiums for 2019 are $189.60, $270.90, $352.20, $433.40, or $460.50, depending on how much a beneficiary’s modified adjusted gross income exceeds $85,000 ($170,000 for a married couple), with the highest premium rates only paid by beneficiaries whose modified adjusted gross incomes are over $500,000 ($750,000 for a married couple). There is also an annual deductible ($185 in 2019) for Part B services. Palmetto GBA, a subsidiary of Blue Cross and Blue Shield, generally processes claims for Part B benefits filed on behalf of Railroad Retirement beneficiaries in the Original Medicare Plan (the traditional fee-for-service Medicare plan). An individual in the Original Medicare Plan should have his or her hospital, doctor, or other health care provider submit Part B claims directly to:

Palmetto GBA Railroad Medicare Part B Office P.O. Box 10066 Augusta, GA 30999-0001 1-800-833-4455 www.palmettogba.com/medicare

Persons with questions about Part B claims under the Original Medicare Plan can contact Palmetto GBA as noted above. 5. Can Medicare Part B premiums increase for delayed enrollment? Yes. Premiums for Part B are increased 10% for each 12-month period the individual could have been, but was not, enrolled. However, individuals age 65 or older who wait to enroll in Part B because they have group health plan coverage based on their own or their spouse’s current employment may not have to pay higher premiums because they may be eligible for “special enrollment periods.” The same special enrollment period rules apply to disabled individuals, except that the group health insurance may be based on the current employment of the individual, his or her spouse or a family member. Individuals deciding when to enroll in Medicare Part B must consider how this will affect eligibility for health insurance policies which supplement Medicare coverage. These include “Medigap” insurance and prescription drug coverage and are explained in the answers to questions six through eight. 6. What is Medigap insurance? Many private insurance companies sell insurance, known as “Medigap,” that helps pay for services not covered by the Original Medicare Plan. Policies may cover deductibles, coinsurance, copayments, health care outside the United States and more. Generally, individuals need Medicare Part A and Part B to enroll, and a monthly premium is charged. When someone first enrolls in Medicare Part B at age 65 or older, he or she has a one-time 6-month “Medigap open enrollment period.” During this period, an insurance company cannot deny coverage, place conditions on a policy, or charge more for a policy because of past or present health problems. 7. Do Medicare beneficiaries have choices available for receiving health care services? Yes. Under the Original Medicare Plan, the fee-for-service Medicare plan that is available nationwide, a beneficiary can see any doctor or provider who accepts Medicare from qualified Railroad Retirement beneficiaries and is accepting new Medicare patients. Those enrolled in the Original Medicare Plan who want prescription drug coverage must join a Medicare prescription drug plan as described in question eight. However, a beneficiary may opt to choose a Medicare Advantage Plan (Part C) instead. These plans are managed by Medicare-approved private insurance companies. Medicare Advantage Plans combine Medicare Part A and Part B coverage, and are available in most areas of the country. An individual must have Medicare Part A and Part B to join a Medicare Advantage Plan, and must live in the plan’s service area. Medicare Advantage Plan choices include regional preferred provider organizations (PPOs), health maintenance organizations (HMOs), private fee-for-service plans and others. A PPO is a plan under which a beneficiary uses doctors, hospitals and providers belonging to a network; beneficiaries can use doctors, hospitals and providers outside the network for an additional cost. Under a Medicare Advantage Plan, a beneficiary may pay lower copayments and receive extra benefits. Most plans also include Medicare prescription drug coverage (Part D). 8. How does Medicare Part D (Medicare prescription drug coverage) work? Medicare contracts with private companies to offer beneficiaries voluntary prescription drug coverage through a variety of options, with different covered prescriptions and different costs. Beneficiaries pay a monthly premium (averaging about $33 in 2019), a yearly deductible (up to $415 in 2019) and part of the cost of prescriptions. Those with limited income and resources may qualify for help in paying some prescription drug costs. The Affordable Care Act requires some Part D beneficiaries to also pay a monthly adjustment amount, depending on a beneficiary’s or married couple’s modified adjusted gross income. The Part D income-related monthly adjustment amounts in 2019 are $12.40, $31.90, $51.40, $70.90, or $77.40, depending on the extent to which an individual beneficiary’s modified adjusted gross income exceeds $85,000 ($170,000 for a married couple), with the highest amounts only paid by beneficiaries whose incomes are over $500,000 ($750,000 for a married couple). To enroll, individuals must have Medicare Part A and live in the prescription drug benefit plan’s service area. Beneficiaries can join during the period that starts three months before the month their Medicare coverage starts and ends three months after that month. There may be a higher premium if an individual does not join a Medicare drug plan when first eligible. A beneficiary can generally join or change plans once each year during an enrollment period from October 15 through December 7. Drug coverage would then begin January 1 of the following year. In most cases, there is no automatic enrollment to get a Medicare prescription drug plan. Individuals enrolled in Medicare Advantage Plans will generally get their prescription drug coverage through their plan. 9. Where can I get more information about the Medicare program? General information on Medicare coverage for Railroad Retirement beneficiaries is available on the RRB’s website, RRB.gov, under the Benefits tab (Medicare) or by contacting an RRB field office toll-free at 1-877-772-5772. More detailed information on Medicare’s benefits, costs, and health care options are available from the Center for Medicare & Medicaid Services (CMS) publication Medicare & You, which is mailed to Medicare beneficiary households each fall and to new Medicare beneficiaries when they become eligible for coverage. Medicare & You and other publications are also available by visiting Medicare’s website, Medicare.gov, or by calling the Medicare toll-free number, 1-800-MEDICARE (1-800-633-4227).

Every three years, the Railroad Retirement Board’s chief actuary conducts a study of the longevity of its annuitants, as part of a valuation of future revenues and benefit payments. The following questions and answers summarize the results of the most recent longevity study.

1. What were the study’s findings on the life expectancy of retired male railroaders?

The most recent data reflected a continued improvement in longevity. Using data through 2016, the study indicated that, on the average, a male railroader retiring at age 60 can be expected to live another 22.5 years, or 270 months. Studies done three, six and nine years ago indicated life expectancies of 22.4, 21.9 and 21.3 years, respectively, for this category of beneficiary. The study also indicated that a male railroader retiring at age 62 can be expected to live another 20.8 years (approximately 250 months), while the previous three studies indicated life expectancies of 20.7, 20.1 and 19.6 years, respectively. A male railroader retiring at age 65 can be expected to live another 18.3 years (approximately 220 months). The previous studies indicated life expectancies of 18.2, 17.7 and 17.1 years, respectively, for this category of beneficiary.

2. How did these life expectancy figures compare to those of disabled annuitants?

As would be expected, disabled annuitants have a shorter average life expectancy than those who retire based on age. At age 60, a disabled railroader has an average life expectancy of 18 years, or 4.5 years less than a nondisabled male annuitant of the same age. Studies done three, six and nine years ago indicated life expectancies of 17.7, 17.2 and 16.4 years, respectively, for this category of beneficiary. Nonetheless, the difference in life expectancy at age 60 between disabled annuitants and annuitants who retire based on age has remained relatively stable, ranging between 4.5 and 4.9 years.

3. Are women still living longer than men?

In general, women still live longer than men. This is shown both in the Railroad Retirement Board’s life expectancy studies of male and female annuitants and by other studies of the general United States population.

For example, at age 60 a retired female railroader is expected on the average to live 25.6 years, 3.1 years longer than a retired male railroader of the same age; and at age 65, a retired female railroader is expected on the average to live 21.1 years, 2.8 years longer than her male counterpart. Spouses and widows age 65 have average life expectancies of 21 years and 19 years, respectively.

4. Can individuals use life expectancy figures to predict how long they will live?

Life expectancy figures are averages for large groups of people. Any particular individual’s lifetime may be much longer or shorter than the life expectancy of his or her age and group.

According to the study, from a group of 1,000 retired male employees at age 65, 933 will live at least 5 years, 822 at least 10 years, 658 at least 15 years and 448 at least 20 years. Of female age annuitants at age 65, 578 will be alive 20 years later.

5. Where can I access the Railroad Retirement Board’s longevity study?

The entire longevity study is available on the RRB’s website, RRB.gov, under the Financial and Reporting tab (Financial, Actuarial and Statistical).

If you are thinking of retiring within the next five years, you may want to consider attending a pre-retirement seminar hosted by the Railroad Retirement Board (RRB). Designed for railroad employees and spouses planning to retire, the pre-retirement seminars the RRB offers familiarize attendees with the retirement benefits available to them, and also guide them through the application process. Sponsored by the Office of the Labor Member, seminars are held at a number of locations annually. RRB field service representatives conduct each pre-retirement seminar using a PowerPoint slide presentation covering the various benefits provided to retired rail workers and their families. Attendees receive a program booklet of this presentation with detailed side notes and fact sheets. In addition to the program booklet, seminar attendees receive a retirement kit full of informational handouts and other helpful materials. Online and downloadable versions of items included with seminar kits are available on the RRB’s educational materials webpage. Registration is required to ensure accommodations and materials for all attendees.

Unless otherwise noted, pre-retirement seminars begin at 8:30 a.m. and are held over the course of four hours. (Doors open for attendees 30 minutes before the seminar start time.)

Security screening is required for seminars hosted inside any federal buildings. Bring a current, valid photo ID (issued by state or federal government); no weapons are permitted.

Parking fee for seminars marked with *.

Attendees are encouraged to bring original records (or certified copies) of documents required in order to file a Railroad Retirement application (such as proof of age, marriage or military service), along with an additional copy of each item to leave with field service staff.

Please inform the RRB if you sign up for a seminar and become unable to attend.

Can’t attend a seminar, but still interested in learning about the Railroad Retirement program and application process? Please contact the RRB via the Field Office Locator or by calling toll-free (1-877-772-5772) for pre-retirement information or to schedule an appointment for individual retirement counseling at your local RRB field office. Here are the scheduled dates:

March 22, 2019: George H. Fallon Federal Building, 31 Hopkins Plaza, Room G-33 (ground level), Baltimore, Maryland*

March 22, 2019: West Covina Library, 1601 West Covina Parkway, West Covina, California* (9 a.m. start time)

March 29, 2019: Birmingham/Jefferson Convention Complex, 2100 Richard Arrington Jr. Boulevard North, East Meeting Rooms D/E, Birmingham, Alabama*

March 29, 2019: Maidu Community Center, 1550 Maidu Drive, Roseville, California

April 5, 2019: Country Inn & Suites, 4500 Circle 75 Parkway, Atlanta, Georgia

April 5, 2019: Hilton Garden Inn (Richmond Airport), 441 International Center Drive, Sandston, Virginia

April 12, 2019: Ronald V Dellums Federal Building, 1301 Clay Street – North Tower, 5th Floor (Room H), Oakland, California*

April 12, 2019: Drury Inn & Suites, St Louis Forest Park, 2111 Sulphur Avenue, St Louis, Missouri

In a recent decision (Wisconsin Central Ltd., et al v. United States), the U.S. Supreme Court ruled that non-qualified stock options granted to railroad employees are not considered compensation under the Railroad Retirement Tax Act of 1937, and are, therefore, not subject to taxation. As a result, certain railroad employers and employees who previously paid railroad retirement taxes based on the exercise of such stock options may be eligible for tax refunds through the Internal Revenue Service (IRS). Railroad employees and railroad retirement annuitants considering filing for such a tax refund should know that doing so may reduce the amount of their total creditable railroad compensation. Under the Railroad Retirement Act (RRA), creditable compensation is a factor in the computation of a railroad retirement annuity. A reduction in compensation could cause a reduction in an annuitant’s monthly benefit rate, and may result in an overpayment. For active employees, a change in creditable compensation may impact any estimated annuity amounts they were previously given by the Railroad Retirement Board (RRB). At this time, the RRB is able to provide guidance to only a select group of individuals trying to determine if their total creditable railroad compensation will be reduced and/or if their annuity amounts will change as a result of claiming refunds of taxes paid on non-qualified stock options. That group is comprised of those individuals who have been identified by their railroad employers as employees whose regular earnings met the maximum compensation taxable caps without the inclusion of the stock option payment. In those cases, if the employees file claims for refunds of taxes paid on the stock option payment, payment of the refund will not impact their annuity rate computations. Employees who believe they are members of this group should review their consent letters to confirm whether they have been reported by their employers to be a “Medicare Tax Only” employee. If you are uncertain whether you are a “Medicare Tax Only” employee, please contact your railroad employer. Employees may also call the RRB’s toll-free number at 877-772-5772 if there are any other questions. The RRB is currently unable to provide guidance to individuals not in the above group. The agency’s three-member board (appointed by the President with the advice and consent of the Senate, and representing rail labor, rail management and the public interest) has the authority to determine what effect, if any, the court’s decision will have on the RRB’s administration of the RRA. However, the position of chairman of the board is currently vacant, and the management member of the board must recuse himself from this issue as he previously worked for a railroad and received non-qualified stock options. The labor member of the board alone lacks statutory authority to make a decision, as a two-member quorum is required by law. It is expected that in the first quarter of 2019, the agency will get a three-member board in place that will be able to make policy decisions related to this matter. The RRB is currently in discussions with the IRS to determine if it is possible to hold open the period for railroad employees and retirees to file claims for tax refunds until such time as the RRB gets a three-member board in place. The RRB would then be better able to provide information regarding the effect on RRB benefits to those needing assistance. Read more about how to apply for the refunds and court decision.

Last July, the Railroad Retirement Board (RRB) mailed approximately 450,000 new Railroad Medicare cards with new Medicare Numbers. The new Medicare Numbers, which are unique to each person with Railroad Medicare and do not contain Social Security Number (SSNs), replace the former Health Insurance Claim Numbers (HICNs). Providers can bill claims to Medicare with either a HICN or a new Medicare Number through December 31, 2019.

Last July, the Railroad Retirement Board (RRB) mailed approximately 450,000 new Railroad Medicare cards with new Medicare Numbers. The new Medicare Numbers, which are unique to each person with Railroad Medicare and do not contain Social Security Number (SSNs), replace the former Health Insurance Claim Numbers (HICNs). Providers can bill claims to Medicare with either a HICN or a new Medicare Number through December 31, 2019.