Notice from John Bragg, the RRB labor member

Brothers and Sisters,

John Bragg

It is hard to believe that 2020 is in the rearview mirror and we are already approaching the mid-point of 2021. The Railroad Retirement Board (RRB) is still operating in a remote capacity with field offices closed to the public. Hopefully, in the not too distant future, I will be writing to advise you of plans for getting back to normal operations. Today, however, I am writing to share a friendly reminder with you about action which every active employee should take on an annual basis – and may be of particular importance this year to some, in light of the unique work circumstances many encountered.

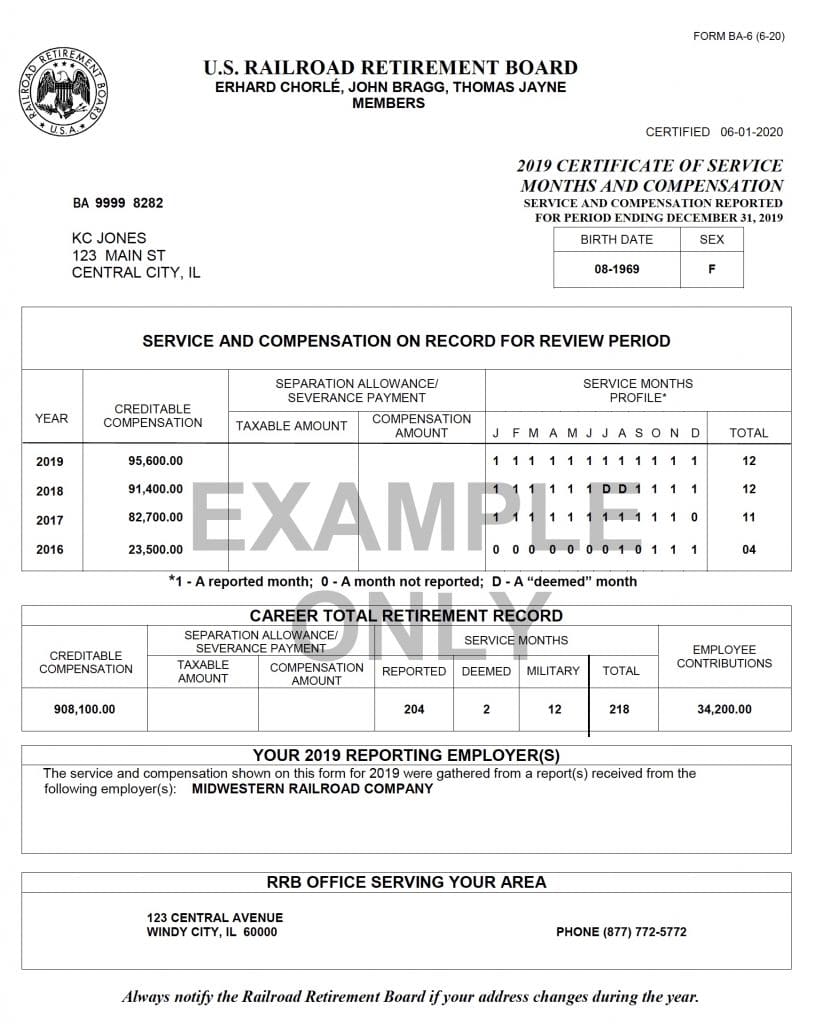

Each year, on or before the last day of February, employers must report service and compensation for each employee who performed compensated service in the preceding calendar year. The RRB, in turn, credits the service and compensation records of individual employees based upon these reports and in June of every year, the RRB releases Form BA-6 to each employee for which compensated service for the preceding year was reported. The Form BA-6 contains the information recently reported for the preceding year, as well as the information reported for three preceding years. For example, the Forms BA-6 which will be released by the RRB in mid-June of 2021 will contain service and compensation reported for the years 2017 through 2020. Regardless of the amount earned, the amount of compensation shown on the Form BA-6 will always be limited by the maximum creditable Tier I compensation amount for the calendar year. For calendar years 2017 through 2020, the maximum amounts creditable are $127,200, $128,400, $132,900 and $137,700, respectively. In addition to showing the creditable compensation for the years 2017 through 2020, the Form BA-6 issued in mid-June of 2021 will show the months for which the employer reported railroad service for the employee during the years 2017-2020.

It is critical that individual employees review their annual Forms BA-6 to make sure that all the information contained on the form is accurate. For example, in addition to validating the creditable compensation, it is important to check to see if the employer properly reported the months for which credit was given by the employer for a month of railroad service. Every month for which you believe you should have credit for railroad service should be coded with a “1”. If the code is “0”, you will not receive credit for any railroad service for that month. If the code is “D” then you will receive credit for railroad service pursuant to the rules governing the deeming of service months.

Employees who received pay for time lost, especially as a result of arbitration proceedings, during the years 2017 through 2020 are reminded of the importance of checking their Forms BA-6. RRB regulations at 20 C.F.R. § 209.15(b) provide that compensation which is pay for time lost must be reported with respect to the year in which the time and compensation were lost. However, it is not uncommon for the individuals responsible for completing reports of service and compensation to be unfamiliar with how to report pay for time lost, or to lack awareness that the compensation they are reporting reflects pay for time lost. As a result, the compensation is mistakenly reported for the year paid AND the service months for which the time and compensation were lost are not credited as railroad service months. Situations where this is most likely to occur are arbitration decisions resulting in the employee being reinstated with all rights and benefits unimpaired and receiving compensation for lost time.

REMEMBER: The law limits the period during which corrections to service and compensation records may be filed to four years from the date the report was due at the RRB, so it is very important for employees to request a correction within that period of time. Any railroad employee who thinks that the Form BA-6 contains an error should be certain to follow the directions on how to file with the RRB a protest of the information contained on the Form BA-6.

Related News

- Senate Strikes Down Spending Bill’s Harmful AI Provision

- Razor blade found on brake wheel

- Coming Soon: SMART-TD Voluntary Income & Life Protection (VILP) Program

- Senate Passes Tax Bill Without Including Railroaders

- SMART-TD Honors the Retirement of Brother Greg Hynes: A Visionary, a Fighter, and a Legend

- SMART-TD Calls on U.S. Senate to Support the Cantwell Amendment and Protect Rail Workers

- Yardmaster Protection Act Introduced

- PHOTO GALLERY: 2025 Denver Regional Training Seminar

- Fighting for Stronger Heat Protections for Rail Workers

- Regional Training Seminar Sets (Mile-High) Record in Denver